Manhattan Real Estate Market Update, Mid-Year 2026: A Record Median Meets the New Pied-à-Terre Tax

Manhattan's second quarter was a scarcity market, and on July 1 a new pied-à-terre tax landed on the buyer who drove it. The median sale price set a record, according to Douglas Elliman and Miller Samuel, while closed sales fell and inventory ran about 15% below a year ago. The quarter looked like strength. The tax changed the terms.

So read Q2 for what it was: a scarcity story. The median rose because the mix shifted higher and there was very little to buy, not because a wave of new buyers arrived. That matters now, because the tax lands on exactly the segment that produced the quarter's best numbers, the non-primary, cash-heavy buyer at the top. The first full week of post-tax luxury data came in mixed. Contract volume actually rose from the holiday week before, but only one apartment signed above $10 million, the thinnest such week in more than six months. One week is not a trend. I would rather flag it early than pretend it did not happen.

In plain terms: the Manhattan median hit a record $1,250,000 in Q2, up about 4.2% year over year, according to Douglas Elliman and Miller Samuel. It rose because a higher share of high-end apartments traded against very thin supply, not because more people bought. Luxury listings fell to 796, the fewest in 22 years of tracking. And since July 1, a new annual surcharge of 4% to 6.5% applies to non-primary condos and co-ops valued at $1 million or more.

How much is the pied-à-terre tax, and who pays it?

New York's pied-à-terre tax, Tax Law Article 30-C, took effect July 1, 2026 and applies an annual surcharge of 4% to 6.5% to non-primary condos and co-ops valued at $1 million or more (one-to-three-family homes are covered at $5 million or more). It was signed on May 28 and runs through 2031. It applies only to property that is not the owner's primary residence. Owner-occupied primary homes are exempt, and so are unsold sponsor units and units without a certificate of occupancy.

On apartments, the rate rises with value: 4% from $1 million to $3 million, 5.25% from $3 million to $5 million, and 6.5% above $5 million. What that works out to in dollars depends on a detail the statute left open. The law does not yet specify whether the surcharge is figured on a property's market value or on its much lower New York City assessed value, or whether the brackets are graduated, and the two tax firms I have read decline to publish a worked example for that reason. Those mechanics await Department of Finance regulations. So treat any single dollar figure you see quoted today as an estimate, not a settled bill.

In more than 20 years advising Manhattan buyers, I have not seen a tax kill demand for a scarce asset. What a tax like this usually does is reprice it. A buyer who was going to pay $6 million now underwrites the surcharge into the offer, so some of the cost lands on the seller over time. Foreign and pure second-home buyers feel it most. Buyers who can claim New York as a primary residence are exempt and now hold a quiet advantage. If you are structuring a purchase this year, ownership and residency planning is no longer a footnote. It is part of the price.

Why the median set a record while sales fell

The benchmark reports tell the scarcity story plainly. Douglas Elliman and Miller Samuel put the Q2 median at a record $1,250,000, up about 4.2% year over year, with the average at $2,113,806 and price per square foot at $1,694. Closings fell about 6.3% to 2,849, and listing inventory dropped 15% to 7,049, with new-development listings down 62%. The share of sales above $1 million reached 57.9%, which Miller Samuel calls the highest on record, and 11.9% of sales closed above ask, up from 7.1% a year earlier. Corcoran, using a different methodology, counted signed contracts up about 5% to 3,477, a multi-year high for a second quarter. Fewer apartments changed hands, but the ones that did skewed higher, and that is what carried the median.

| Metric | Q2 2026 | Read |

|---|---|---|

| Median sale price | $1,250,000 (+4.2% YoY) | A record, on a shift toward higher-priced product against thin supply. |

| Average sale price | $2,113,806 (+0.7%) | Lifted by large-format, upper-tier closings. |

| Price per sq ft | $1,694 (+2.7%) | Up 2.7%, roughly tracking the median. |

| Closed sales | 2,849 (−6.3%) | Fewer deals closed; the gain is price, not volume. |

| Listing inventory | 7,049 (−15%) | Resale down 7%, new development down 62%. |

| Sales above $1M | 57.9% | Highest share on record; confirms the shift to higher-priced product, not a wider buyer pool. |

| Closings above ask | 11.9% | Up from 7.1% a year ago; real competition where product is scarce. |

The top: a strong quarter, then a softer first week

Through June, the high end did the heavy lifting. Compass, which counts signed contracts, reported $10 million to $20 million contract volume up about 38.6% year over year and $20 million-plus signings up about 25%. Elliman's closed luxury median, a lagging measure, tells a quieter story: it slipped about 1.1% to $6,451,500, so the strength was in the number of contracts, while prices at the top held rather than climbed. The luxury entry point sat around $4,450,000. Underneath all of it is supply. Just 796 luxury listings, the fewest in 22 years, with no new Billionaires' Row supertall launching sales this year.

Then July arrived. In the first full week after the tax took effect, Olshan Realty counted 29 contracts signed at $4 million and above, totaling $182 million. That was up from 15 the July 4 holiday week before, so broad luxury volume did not fall. What fell was the very top: only one deal signed above $10 million, the thinnest $10 million-plus week in more than six months. The typical property had been on the market over a year and took about a 6% cut. It is one week, it followed a holiday, and some of it is timing. But it is the first read on a taxed market, and the softness showed up exactly where the tax bites hardest.

Where product is genuinely scarce, the pipeline argues for repricing rather than a real correction. Billionaires' Row is running low on trophy supply: 111 West 57th Street is near sellout, resales at the Aman on Fifth Avenue trade at some of the city's highest prices per foot, and no new supertall is launching sales this year. When a tax adds carrying cost to a segment that cannot be replenished, repricing is likelier than retreat. For the building-by-building view of what is actually left, and why so little of it is coming, see The Trophy Condo Pipeline and our Manhattan Ultra-Luxury Market Report.

Rates and the backdrop

Financing did not get easier. The 30-year fixed sits near 6.49%, about where it was through the spring and a little below a year ago. The Federal Reserve held its benchmark at 3.50% to 3.75% in June and struck a hawkish tone, with the next decision due July 29, so a near-term cut is not the base case. What keeps the top liquid is not credit. It is wealth. The S&P 500 is trading near record levels, and well above $3 million most Manhattan purchases are all-cash. That is why the high end can absorb a rate that would stall a financed buyer, and it is why a tax that raises the annual cost of holding an apartment matters more this year than the cost of borrowing to buy one.

What this means for buyers and sellers

For pied-à-terre and foreign buyers. Model the surcharge before you bid, and get ownership and residency structuring right up front. On a $5 million-plus apartment the annual cost is large enough to change the number you should offer, and it is a fair negotiating point, because the seller now shares that reality.

For luxury buyers who can claim a primary residence. You are exempt from the surcharge, and you are competing against fewer taxed buyers for the same scarce product. That is a real edge at the top this year.

For buyers below the top. Selection is widest under $2 million, and the leverage is in aged listings. If an apartment is turnkey and correctly priced, expect company. If it has sat 90 days or longer, the conversation moves your way. Ask me for the current list of 90-day-plus listings in your target neighborhood.

For sellers. A record median is not permission to overreach. Pricing to the evidence in the first weeks still decides the outcome, and if your buyer pool is non-primary, price in the fact that their carrying cost just went up. At the very top, scarcity is still on your side.

Want the mid-year read for a specific building, price band, or your own tax exposure? I will pull live comps, stale inventory, and contract activity, and model the surcharge into an offer.

Methodology: Q2 2026 quarterly figures are from Douglas Elliman / Miller Samuel and Corcoran; luxury contract-band figures from Compass; weekly luxury contract data from Olshan Realty; mortgage rates from Freddie Mac (week of July 9, 2026); the pied-à-terre surcharge from NY State Tax Law Article 30-C, effective July 1, 2026. Douglas Elliman / Miller Samuel and Corcoran use different methodologies and are not directly comparable, and signed-contract counts (a leading measure) are not comparable to closed-sale figures (a lagging one). The tax base and bracket mechanics are subject to Department of Finance regulation; confirm your own exposure with tax and legal counsel. Last updated July 13, 2026 by Anthony Guerriero, Manhattan Miami Real Estate.

Manhattan Condo Market Report, Q2 2026

Q2 2026 delivered the clearest signal of the cycle: Manhattan is not moving as one market. The top is booming. By most accounts the luxury segment posted its strongest quarter in years, driven by scarce trophy inventory, cash-heavy demand, and a decisive flight to quality — while the rate-sensitive middle of the market continued to trade selectively and reward only realistic pricing. The result is a widening gap between the high end and everything below it.

What makes the quarter notable is not broad price inflation but concentration. Pricing strength is being produced by mix and scarcity: a higher share of large-format, high-end transactions against a historically thin supply of comparable product. Buyers remain disciplined, yet when an asset is finished, well located, and correctly priced, the best inventory is absorbing quickly and, at the very top, competitively. For sellers, Q2 was a discipline test. For luxury sellers, it was the best window in years.

In plain terms: Q2 pricing held firm because the upper end carried more weight. Luxury contract volume surged while high-end supply fell to its lowest level in two decades, and a thin new-development pipeline limited buyer choice. The market remains liquid for properly priced product — and much less forgiving for listings that enter above the evidence.

The luxury surge: the top of the market is booming

The defining story of Q2 2026 is strength at the top. Early quarterly reporting points to one of the strongest luxury quarters Manhattan has seen in years. Contract volume in the $10M–$20M band rose an estimated 54.5% year over year, and the $20M-plus bracket climbed roughly 33.3%, even as the broad-market median settled near $1.25M (up about 4.2%). The engine is not cheap money — it is scarcity, wealth, and a durable preference for New York trophy assets as a store of value.

Supply is the accelerant. Luxury inventory is down roughly 40% year over year and, by several accounts, sits at its lowest level since 2004. With so few trophy residences available and a new-development pipeline that cannot replace them quickly, qualified buyers are competing for a shrinking pool of best-in-class product. Weekly signed-contract activity at the high end has been running at its fastest pace in over a year. Notably, the surge has held up despite the arrival of a new second-home / pied-à-terre tax — the widely discussed “Mamdani effect” — which the market has so far absorbed rather than repriced.

The strength was not uniform through the quarter, however. Several brokerages noted that signed-contract activity above $5M cooled in the weeks after the new tax was announced, with the sharpest hesitation at the ultra-luxury end — a sign some buyers are recalibrating. The headline numbers are strong, but part of that strength likely reflects demand pulled forward ahead of the tax, which makes Q3 the real test.

It is also a top-heavy story. Broad luxury demand was steadier than the headlines suggest: signed contracts at $4M and above ran roughly flat year over year — Olshan Realty counted 126 contracts signed at $4M+ in June, against 124 in the same period a year earlier. The real acceleration was concentrated at the very top, where $10M+ contract volume jumped sharply. In other words, the quarter’s strength was less about broad luxury exuberance and more about a scarcity-driven surge in trophy and ultra-luxury product.

| Price band | YoY change in contract volume | Read |

|---|---|---|

| $5M–$10M | Materially higher | Broad luxury demand strengthened across the entry-trophy tier. |

| $10M–$20M | ~+54.5% | The standout band — the clearest evidence of a booming high end. |

| $20M+ (ultra-luxury) | ~+33.3% | Trophy demand deepened even as available product hit multi-decade lows. |

| $4M+ (broad luxury) | ~Flat YoY | Olshan counted 126 contracts at $4M+ in June vs. 124 a year earlier — steady, not surging. |

| Luxury inventory | ~-40% YoY | Lowest since 2004; the central driver of the high-end surge. |

At the very top, pricing is set by pedigree and scale. Trophy and branded-residence product is transacting in a roughly $4,000–$9,500 per square foot range, with Billionaires’ Row and the marquee supertalls clearing $5,000+ per square foot. Branded residences — Aman, and the other flagged flagships — continue to command the sharpest premiums and some of the quarter’s most competitive resale activity. For the full building-by-building read on $10M+ inventory, recent trades, and contract activity, see our Manhattan Ultra-Luxury Market Report.

Broad-market benchmarks

| Metric | Q2 2026 read | Interpretation |

|---|---|---|

| Median sale price | ~$1.25M–$1.3M | Up ~4–7% year over year across the major indices; near record highs. |

| Average sale price | ~$2.2M | Up ~5–6% YoY to its second-highest level on record, lifted by large-format upper-tier closings. |

| Signed contracts | ~3,477–3,679 | Up ~5–11% YoY to a multi-year second-quarter high; demand held despite higher rates and the new tax. |

| Average days on market | ~115 days | Improved year over year for the eighth straight quarter. |

| Closed sales | ~3,040 | Healthy volume, though performance varies sharply by segment. |

| Luxury inventory | Down ~40% YoY | At a two-decade low; the primary support for top-of-market pricing. |

| New development pipeline | Launches ~-37% YoY | Roughly 160 units, about half the typical second quarter; replacement-quality product stays scarce. |

Condos vs. co-ops, the practical split

Condominiums remain the cleaner liquidity vehicle for international buyers, investors, and purchasers who want optionality around financing, ownership structure, leasing, and resale. That flexibility — and the fact that most trophy new-development product is condo — continues to support the condo premium and concentrates the luxury surge there. Co-ops remain more sensitive to board standards, financing limits, and local end-user demand. The result is not that co-ops are weak; it is that co-op liquidity is more selective and building-specific.

| Segment | Demand profile | Pricing implication |

|---|---|---|

| Trophy & ultra-luxury ($10M+) | Booming — cash-driven, global, and supply-starved. | Double-digit contract growth; scarcity commands full premiums for scale, view, and pedigree. |

| Move-in-ready condos | Strongest broad-market depth, especially in prime buildings. | Best chance of early, competitive activity when priced correctly. |

| Prime co-ops | Stable end-user demand in the best buildings. | Pricing holds when financials, condition, and board profile are strong. |

| Aspirational listings | Buyer resistance rises after the first several weeks. | Price reductions are more likely once listings cross the stale threshold. |

New development, the supply story continues

The Q1 theme of limited new development did not reverse in Q2 — it intensified the luxury squeeze. New sponsor launches remain far below long-term norms, and the cost of creating comparable inventory has moved higher. That matters most at the top: Manhattan’s best condo product is expensive to replace, politically difficult to entitle, and slow to deliver, so the trophy shortage cannot resolve on any near-term horizon.

What Q2 means for buyers and sellers

For luxury buyers. Competition at the top is real and rising. With trophy supply at a two-decade low, the best $10M+ residences are trading quickly and at full value — waiting for a discount cycle is the higher-risk strategy this year.

For buyers below the top. The best opportunities are still found where pricing has aged, not where quality is highest. If the apartment is turnkey, scarce, and correctly priced, expect competition. If it has been sitting for 90 days or longer, the conversation changes.

For sellers. Q2 rewarded launch discipline — and, at the high end, rewarded sellers outright. The first several weeks remain the most important window. A realistic asking price, strong presentation, and direct comparison to competing inventory matter more than ever.

Want the Q2 read for a specific building, price band, or neighborhood? We can pull current comps, stale inventory, and live contract activity.

Methodology: Q2 2026 figures are preliminary and reflect early quarterly market reporting (Corcoran, Douglas Elliman / Miller Samuel, Compass, Brown Harris Stevens, Olshan Realty, and UrbanDigs) together with Manhattan Miami’s analysis of transaction mix, inventory constraints, and buyer behavior. Luxury contract-band and inventory figures are directional and subject to revision as final brokerage-reported data and public records settle; final figures may vary.

Private market intelligence · Delivered in 24 hours

Get the Manhattan numbers that aren't in the report

A confidential read on pricing, absorption, and where there is room to negotiate for your building or target, prepared by an advisor rather than an algorithm. No obligation.

Prefer to message us? WhatsApp +1 646 376 8752

Before you reach out

- I am only exploring.

- That is the right time. Most of our clients start a year or more before they buy, and early conversations are how we learn what actually fits before anything is on the table.

- Will I end up on a call list?

- No. One advisor reads your note and replies personally. You set the pace, and you can ask us to pause at any point.

- Is the off-market inventory real?

- Yes. A meaningful share of trophy trades never reaches a public portal. We share what is genuinely available and quietly listed, not recycled listings.

- I already work with a broker.

- Understood. Many clients use us for a second, cross-market read on pricing and timing. If you are represented, tell us and we will keep it strictly informational.

Ready sooner? Begin a private advisory conversation. Selling instead? See selling your home.

Manhattan Real Estate Market News

Manhattan buyers signed contracts at the fastest pace in more than a year, with 1,162 deals signed over the trailing 30 days as active inventory fell 8.5% from a year ago. Disciplined seller pricing and mortgage rates near 6.5% are driving the activity, while listings above $4 million still close below ask. Here is the weekly read on where the market stands and what it means if you are buying or selling now.

In plain terms: Manhattan recorded 1,162 signed contracts over the last 30 days, up 10.1% year over year, with 302 new contracts this week, up 29.6%. Active inventory is 6,761 listings, down 8.5% year over year. The 30-year conforming mortgage rate is near 6.56%, about 0.36 points below a year ago.

Supply is the other half of the story, and it is getting leaner. Active inventory sits at 6,761 listings, down 8.5% from a year ago even as a normal wave of spring listings arrived. The market is sorting itself by discipline. About 40% of active listings have now been available for 90 days or longer, the stale segment that signals mispricing. Correctly priced homes are moving quickly while overpriced ones sit, according to live contract and inventory data from UrbanDigs for the week of May 25, 2026.

The Upper West Side is the clearest example of the citywide story playing out at the neighborhood level. Condo price per square foot reached $1,752 on a two-month rolling median, up 11.2% from a year ago, while co-op pricing held at $1,194. Closed sales in the neighborhood ran up 34.1% year over year with a median sale price of $1.7 million, a 20.3% annual gain. In more than 20 years advising buyers and sellers in Manhattan, the cleanest tell of a healthy neighborhood is exactly this: scarce condo product bid up while co-op supply rebuilds and still clears. Buyers chasing turnkey condos are competing; buyers open to co-ops have more room.

| Metric | Condo | Co-op |

|---|---|---|

| Price per sq ft (rolling median) | $1,752 (+11.2% YoY) | $1,194 |

| Active listings | 164 | 263 (+43.7% YTD) |

| Median sale price (neighborhood) | $1.7M, up 20.3% YoY | |

| Days on market (neighborhood) | 65 days, down 22.6% MoM | |

Price behavior splits sharply by tier. In the $1 million to $2 million band, 28% of sales closed above ask and 23% closed at ask, a sign of genuine competition. Above $4 million, the picture flips: 60% of those sales closed below ask, so well-capitalized buyers at the top retain leverage. Financing is a tailwind again, with the 30-year conforming rate near 6.56% and jumbo near 6.64%, both roughly 0.36 to 0.41 points below year-ago levels. That matters most to the financed tiers below $4 million. For context on the longer arc, see our Q1 2026 snapshot and Q4 2025 year-end review further down this page.

What this data means for buyers and sellers

For buyers. Below $2 million, expect competition and move decisively, because well-priced homes are clearing fast. Above $4 million, you hold leverage, since most sales there close under ask. The smartest plays right now are the 90-day-plus listings, where sellers are most likely to negotiate.

For sellers. Realistic pricing wins. Move-in-ready homes priced to the market are signing quickly, while overpriced listings join the 40% that have sat 90 days or longer. The cost of testing a high number is months of lost time and a weaker eventual price.

Sellers: get a data-backed price range built to move in under 60 days. Buyers: get this week's negotiable listings.

Tracking a specific building or price point? We pull live contract and days-on-market data for private clients. Message us on WhatsApp at +1 646 376 8752.

Manhattan Real Estate Market News: Frequently Asked Questions

Are Manhattan real estate prices dropping?

No, Manhattan prices are not broadly dropping. As of the week of May 25, 2026, signed contracts are up 10.1% year over year and Upper West Side condo price per square foot is up 11.2%. The softness is confined to overpriced listings that have sat on the market for 90 days or longer, which now make up about 40% of active inventory.

Is now a good time to buy property in NYC?

For financed buyers below $4 million, conditions have improved. Mortgage rates near 6.56% are about 0.36 points below a year ago, and selection is widest in that range. For buyers above $4 million, 60% of recent sales closed below ask, so there is room to negotiate. The main constraint is scarce, move-in-ready inventory, which rewards decisive buyers.

What is the NYC real estate prediction for 2026?

The current trajectory points to firm pricing and rising transaction volume into the second half of 2026, supported by tight inventory, easing mortgage rates, and strong contract activity. The trophy tier at the very top of the market is expected to stay the most supply-constrained segment, keeping pricing power with sellers of scarce, finished product.

Why does this report track signed contracts instead of closings?

Closed sales reflect decisions made 60 to 90 days earlier, so they describe the past. Signed contracts reflect what buyers are doing right now, which makes them the more accurate real-time signal in a fast-moving market. This is why our weekly Manhattan real estate market news leads with contract activity.

Methodology: weekly figures cover Manhattan condominiums and co-ops and are compiled from live UrbanDigs contract, inventory, and pricing data for the week of May 25, 2026. Quarterly benchmarks from Douglas Elliman / Miller Samuel. Last updated June 8, 2026 by Anthony Guerriero, Manhattan Miami Real Estate.

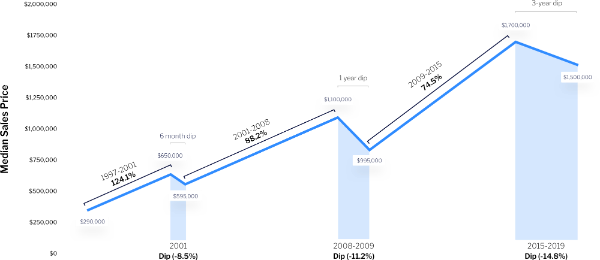

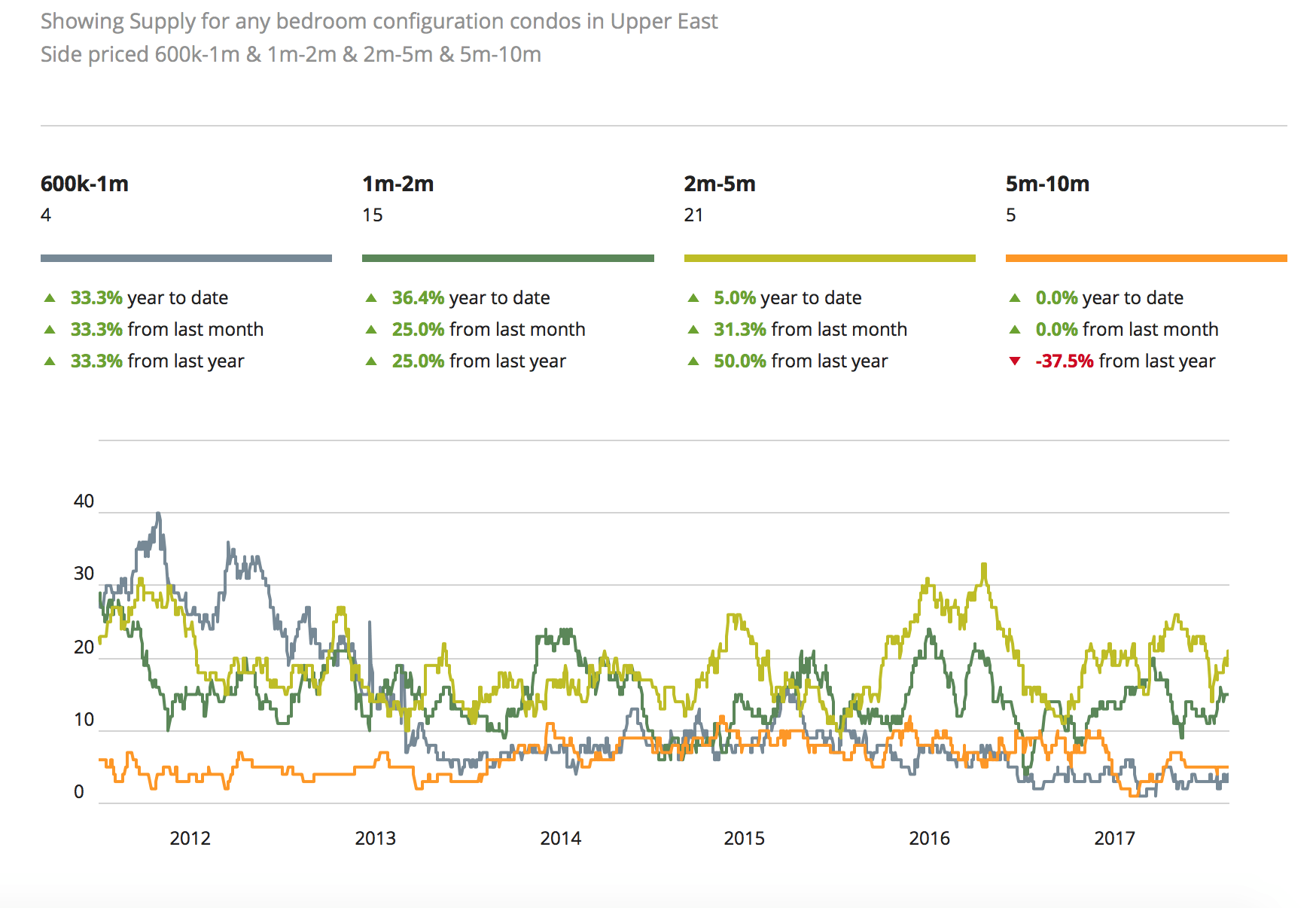

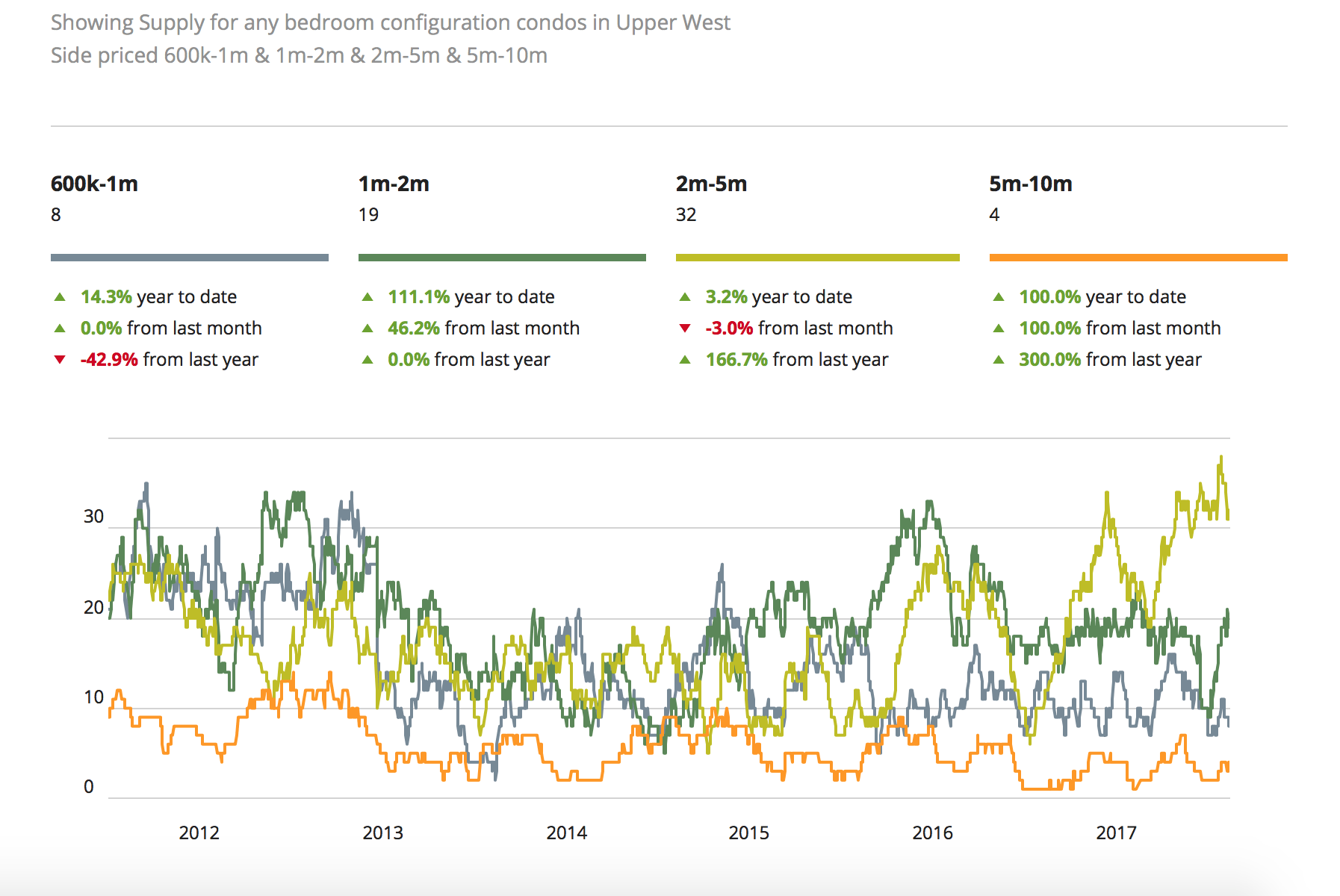

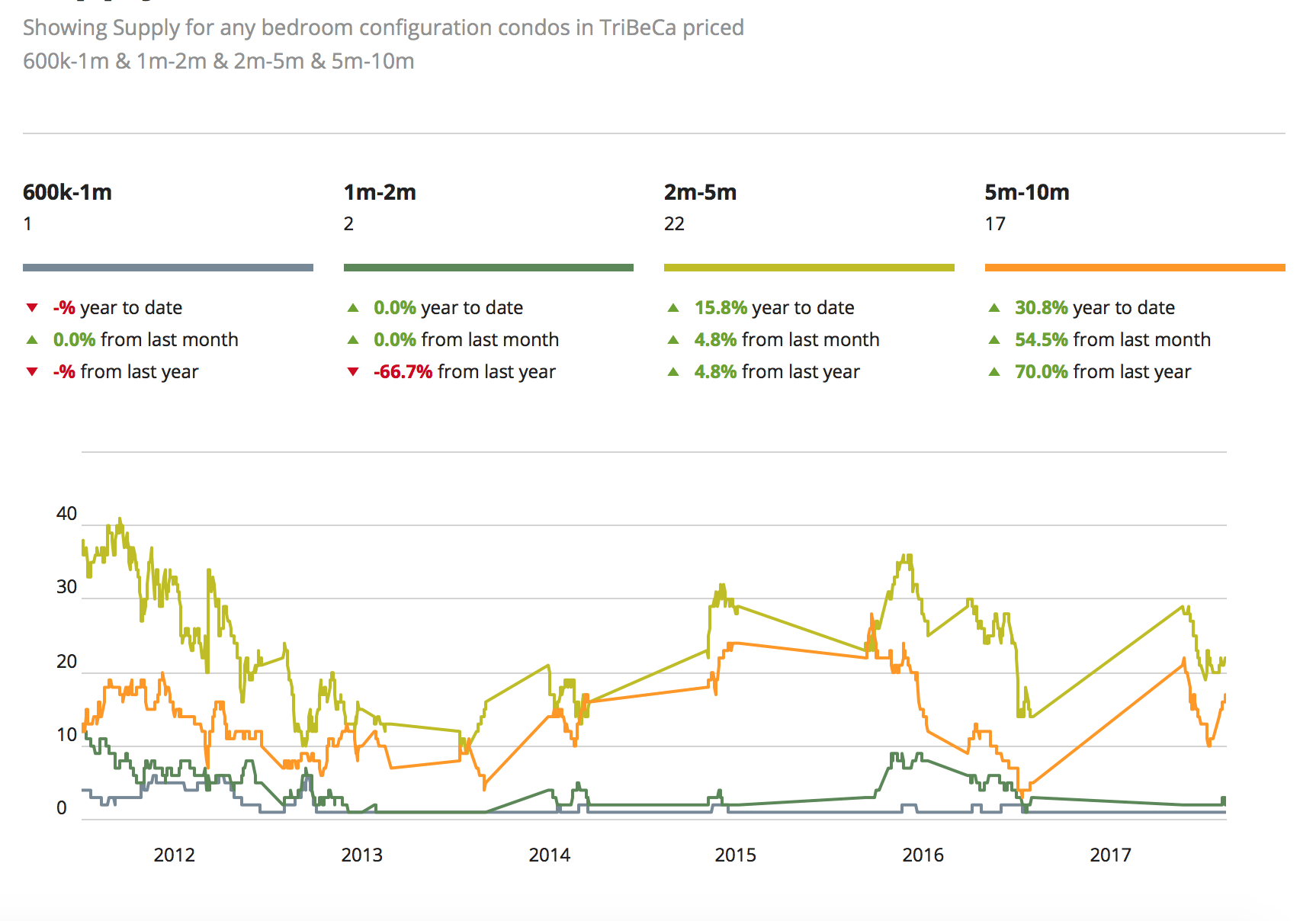

Manhattan Neighborhood Home Price Resilience

2008 crisis, 2019 peak, and 2022-2023 correction by submarket, Upper East Side, Tribeca, and key neighborhoods

| Neighborhood | 2008 Drop | Recovery to 2019 | 2022-2023 Correction | Resilience |

|---|---|---|---|---|

| Upper East Side | −12% | +38% | −5% | High |

| Tribeca | −18% | +72% | −9% | Very High |

| Upper West Side | −11% | +32% | −6% | High |

| SoHo / West Village | −15% | +58% | −8% | High |

| Midtown / Murray Hill | −22% | +24% | −14% | Moderate |

| Downtown / FiDi | −16% | +44% | −10% | Moderate-High |

Source: Manhattan real estate transaction data, Miller Samuel / Douglas Elliman market reports. Figures represent median PPSF change across each cycle for each submarket. Individual buildings vary.

Q1 2026, Editorial Introduction

Q1 2026 was not a broad-based recovery in Manhattan. It was a selective, wealth-driven condo market in which constrained new development supply, a higher mix of large-format transactions, and durable luxury demand did the work that broad price inflation did not.

For active sponsor inventory and recently delivered Manhattan towers, explore NYC new developments.

The headline numbers tell the story only when read together. Closings rose 1% year over year. Volume rose 4%. Median price rose 9%. The gap between transaction count and pricing is the signal: fewer, larger, better deals are setting the tone, while ordinary inventory continues to clear at ordinary prices.

For global buyers, sellers, and family offices, the practical takeaway is that the top of the market is decoupling from the middle. Capital is concentrating into a narrower band of condo product, boutique, park-adjacent, architecturally significant, downtown trophy. That concentration, not market-wide enthusiasm, is what is producing the pricing strength visible in the Q1 data.

Market Snapshot

- Median Price: $1.28M (+9% YoY)

- Average Price: ~$2.25M

- Average PPSF: $1,972 (+4% YoY)

- Sales Volume: $6.2B (+4% YoY)

- Closings: 2,757 (+1% YoY)

- Active Inventory: ~6,000 units (five-year Q1 low)

- New Development Launches: 81 units (~75% below 10-year average)

- $3M+ Transactions: +10% YoY

- Condo Average: ~$3.16M

- 4BR+ Condo Closings: ~$10.88M / ~$2,965 PPSF

- 4BR+ Condo Contracts: ~$13.32M / ~$3,268 PPSF

Key takeaway: Manhattan is being led by quality, scarcity, and wealth, not by broad-based price inflation.

Contracts, The Real-Time Market Signal

Closings describe the past. Contracts describe the present.

Q1 2026 closings reflect deals largely negotiated in late 2025. To read the live market, the more useful instrument is the contract pipeline. What buyers are committing to today, at what pricing, and at what scale.

The signal from contracts is firmer than the signal from closings. 4+ bedroom condos under contract during Q1 averaged approximately $13.32M and $3,268 PPSF, against closed figures of approximately $10.88M and $2,965 PPSF. The contract book is larger and priced higher than the closing book.

That divergence matters. It indicates that the upper end of the market is, if anything, accelerating into Q2, and that Q2 closing data, when it prints, will likely be stronger than Q1's. Buyers operating with the assumption of a soft market are reading lagging information.

The Condo Market

Condo activity carried the quarter. The average condo closed near $3.16M, well above the all-Manhattan average of roughly $2.25M, reflecting both buyer mix and the relative weakness of co-op velocity at comparable price points.

Pricing strength is concentrated in larger units. 4+ bedroom condos averaged approximately $10.88M closed, at roughly $2,965 PPSF. Forward-looking contract data is firmer still, as discussed above.

The interpretation is straightforward. Buyers with optionality are paying premiums for scale, finish, and irreplaceability. Buyers without that optionality are negotiating.

Luxury, Ultra-Luxury, and Trophy

We define luxury as approximately the top 10% of the Manhattan market, roughly $4M and above. By that definition, luxury volume was the dominant story of Q1: $3M+ transactions rose 10% year over year against essentially flat overall closings.

We do not define ultra-luxury simply as "over $10M." That threshold is too generous. For Manhattan Miami, ultra-luxury generally requires both $10M+ pricing and roughly $4,000+ PPSF. Below that PPSF level, a $10M+ unit is large, not necessarily prime.

Trophy property is a separate category, defined not by price but by the convergence of irreplaceability, view, scale, building pedigree, privacy, and scarcity. There are perhaps several dozen genuine trophy assets in Manhattan at any given time. Q1 2026 confirmed that demand for them is real, deep, and global.

New Development, A Supply Story

The most important Q1 2026 data point is not a closing. It is a launch.

Only 81 new development units launched in Q1, roughly 75% below the 10-year average. This is not a demand problem. It is a supply problem.

Manhattan developers face elevated capital costs, complex land assembly, and a pipeline that was already thinning before 2025. The result is that fresh, high-quality condo product, particularly boutique, park-adjacent, downtown, and architecturally significant projects, is entering the market at a fraction of the pace required to absorb global capital flowing into New York.

This shortage is what supports pricing at the top end. When supply is structurally constrained and demand is not, the pricing math at the upper tiers does not require broad market participation. It only requires the next ten qualified buyers per project.

Notable Trophy Activity

Several Q1 transactions illustrate the pattern.

1122 Madison Avenue. Robert A.M. Stern's Upper East Side limestone condominium recorded strong early contract activity, with reports of 18 of 26 units under contract within weeks at average pricing near $5,439 per square foot. The lease-up pace at that PPSF is the most precise read available on UES trophy demand.

175 Fifth Avenue (Flatiron Building Conversion). The landmark conversion produced reported contracts including units near $24.8M and $30.5M. Buyer willingness to pay landmark-conversion premiums for an irreplaceable building confirms that pedigree is being priced explicitly, not implicitly.

70 Vestry, Tribeca. A reported $57M penthouse sale anchors the case that downtown trophy demand is fully intact. This is not exclusively a Billionaires' Row story. Capital is moving south as well as up.

The dispersion across UES, Flatiron, and Tribeca matters. The trophy market is not a single neighborhood. It is a quality threshold.

Buyer Implications

For buyers operating above $4M, and particularly above $10M, the Q1 data argues against waiting on a broad-market correction. The price action is not coming from speculation. It is coming from constrained supply meeting durable wealth demand. In that regime, the cost of waiting compounds quickly when the next high-quality launch is six to twelve months away.

The contract pipeline reinforces the point. Forward indicators are firmer than closed indicators, which means the buyer who reads only closing data is underwriting a market that no longer exists.

The disciplined move is to underwrite specific assets, not the market average. Best-in-class condo product is trading on its own curve.

Seller Implications

For owners of quality condo product, particularly larger, architecturally distinguished, or view-protected units, Q1 confirms that pricing leverage exists, but only with proper positioning. The market is rewarding scarcity, not optimism. Aggressive list-and-reduce strategies are still being penalized; well-priced, well-presented launches are clearing.

For owners of secondary product, the calculus is different. Median and average pricing have moved, but absorption still depends on realistic pricing into a selective buyer pool.

Q1 2026, Frequently Asked Questions

What is the median Manhattan condo price in Q1 2026?

How many Manhattan condos closed in Q1 2026?

How many new development units launched in Q1 2026?

What is the difference between luxury and ultra-luxury Manhattan real estate?

What were the most notable Manhattan trophy transactions in Q1 2026?

Are Manhattan condo contracts pricing higher than closings?

Closing

The Manhattan condo market entered 2026 narrower at the top and stronger where it counts. Trophy demand is global. New development supply is structurally constrained. Wealth is concentrating into best-in-class assets across both Manhattan and Miami, and the capital corridor between the two cities continues to deepen.

For UHNW buyers and sellers, that combination defines the strategic frame for the rest of the year. The opportunity is not in calling the market. It is in identifying the specific assets where scarcity, quality, and timing converge.

Sources: Corcoran 1Q 2026 Manhattan Real Estate Market Report; SERHANT. Q1 2026 Manhattan Market Report. By Anthony Guerriero, Manhattan Miami Real Estate · April 2026.

Comparing capital flows? Read the parallel Miami market analysis.

Q4 2025, Year-End Review

Executive Summary

Manhattan closed 2025 on stable footing, with pricing remaining firm, inventory constrained, and transaction activity supported by continued strength at the higher end of the market. Despite elevated borrowing costs, demand persisted, particularly among equity-driven buyers less sensitive to financing conditions.

However, beneath these stable headline metrics, the market began to show early signs of segmentation. Entry-level activity softened modestly, while luxury transactions accounted for a growing share of total dollar volume. At the same time, the new development pipeline continued to thin, reinforcing supply constraints that would carry into 2026.

Why We Focus on Contracts

Closed sales reflect decisions made 60-90 days prior.

Signed contracts reflect current buyer behavior.

In a market shaped by:

- interest rate uncertainty

- financial market volatility

- shifting buyer psychology

contracts provide a more accurate indication of near-term direction.

Q4 2025, Market Snapshot

- Contracts signed: Stable to modestly down year-over-year

- Closings: Stable to slightly increased year-over-year

- Median price: Held firm, with modest year-over-year growth

- Inventory: Remained constrained relative to historical norms

- Days on market: Stable, with well-priced properties continuing to transact efficiently

Interpretation

- Pricing remained supported by limited supply

- Demand persisted, particularly at higher price points

- The market showed early signs of divergence across segments

Market Segmentation, Early Signals

Entry-Level Market (Below ~$3M)

- Increased sensitivity to mortgage rates

- Slower pace of transactions

- Greater negotiation and buyer caution

Conclusion:

→ Demand remained present, but increasingly constrained

Luxury Market ($3M+)

- Continued strength in transaction activity

- Growing share of total market volume

- Strong performance in well-located, high-quality assets

Conclusion:

→ Demand remained resilient and less dependent on financing conditions

New Development, A Thinning Pipeline

New development supply continued to contract in Q4 2025.

- Fewer large-scale projects launching

- Greater reliance on boutique developments

- Slower pace of new inventory delivery

In contrast to prior cycles, where individual projects could deliver hundreds of units, the pipeline has shifted toward smaller-scale, more limited releases.

Implication:

→ Future supply constraints were already forming by late 2025

📊 NYC vs Manhattan, A Critical Distinction

Headline New York City data continued to overstate supply conditions relevant to Manhattan buyers.

- Significant unit volume concentrated in Brooklyn and Queens

- Much of that supply below $2M or rental-driven

- Manhattan representing a smaller share of units, but a disproportionate share of value

For Manhattan buyers, the relevant supply pool remained limited.

Inventory, Supporting Pricing

Inventory levels remained constrained throughout the quarter.

- Limited new listings entering the market

- Sellers generally not under pressure

- Reduced competition among listings in prime segments

This environment continued to:

- support pricing stability

- reduce downward pressure

- favor well-positioned properties

Buyer Behavior, Shifting Psychology

Buyer behavior in Q4 reflected a more measured approach.

- Longer decision timelines

- Increased focus on value and positioning

- Greater selectivity across all segments

At the same time:

- High-net-worth buyers remained active

- Equity-driven purchases continued

- Trophy and well-priced assets attracted strong interest

Advisory Perspective

By the end of 2025, the Manhattan market could best be described as:

→ Stable

→ Supply-constrained

→ Beginning to segment

- Entry-level demand showing pressure

- Luxury demand remaining resilient

- Supply dynamics becoming increasingly important

Outlook, Entering 2026

As Manhattan moved into 2026:

- Supply constraints were expected to persist

- Buyer selectivity was likely to increase

- Segmentation between price points expected to widen

Expectation:

→ A transition from a broadly stable market to a more selective and segmented environment

Q3 2025, Deep Dive

Manhattan Condo and Co-op Sales Surge to Two-Year High

The Manhattan real estate market delivered exceptional performance in the third quarter of 2025, with residential sales reaching their highest level in over two years. The market is trending positively, with rising sales and price growth indicating strong momentum.

This comprehensive market analysis examines current trends in Manhattan condos, co-ops, luxury properties, and new developments based on the latest Douglas Elliman market report.

Executive Summary: Manhattan Housing Market Q3 2025

Manhattan’s residential real estate market demonstrated remarkable strength in Q3 2025, with 3,158 closed sales representing a 13.4% year-over-year increase, the strongest quarterly performance since 2023. The Manhattan condo market and co-op sector both posted double-digit sales growth, while median sales prices rose 5.8% to $1,180,000.

Key Manhattan Market Highlights:

-

Manhattan home sales reached 3,158 closings, up 13.4% annually

-

Median Manhattan condo price: $1,650,000 (+2.2% YoY)

Manhattan’s median condo price is significantly higher than the national average, highlighting the substantial disparity in housing costs. -

Median Manhattan co-op price: $870,000 (+3.6% YoY)

Housing costs, including property taxes and maintenance fees, play a major role in overall affordability for buyers. -

Cash transactions dominated at 65.3% of all sales

-

Manhattan luxury real estate inventory declined 16.1% year-over-year

-

New development sales surged 71% annually

Manhattan Condo Market Analysis Q3 2025

Manhattan Condo Sales and Pricing

The Manhattan condo market posted impressive gains in Q3 2025, with 1,407 condo closings, a 16.6% year-over-year increase. This represents the strongest quarterly performance for Manhattan condos in recent years.

Manhattan Condo Market Metrics:

-

Median condo price: $1,650,000, up 2.2% year-over-year

-

Average condo price: $2,651,636, down 5.1% (reflecting unit mix shift)

-

Average price per square foot: $1,998, down 2.3%

-

Higher mortgage rates have led to increased monthly payments for buyers, making homeownership less affordable and influencing some to reconsider their purchase decisions.

-

Days on market: 74 days, down 3.9% annually

-

Condo inventory: 4,064 units, up 8.3%

Nearly 70% of Manhattan condo sales were all-cash transactions during Q3, demonstrating the strong presence of well-capitalized buyers in the market. Sales over $2 million showed particularly robust growth, rising at triple the rate of properties under $2 million.

Manhattan Condo Prices by Bedroom Count

Bedroom TypeMedian Sale Price Q3 2025Year-over-Year ChangeStudio Condos$693,500N/A1-Bedroom Condos$1,135,000N/A2-Bedroom Condos$2,150,000Strong demand3-Bedroom Condos$3,917,500Premium segment4+ Bedroom Condos$6,601,289Luxury tierManhattan Co-op Market Analysis Q3 2025

Manhattan Co-op Sales Performance

The Manhattan co-op market demonstrated strong momentum with 1,751 closings in Q3 2025, representing an 11.0% year-over-year increase. Co-op sales growth outpaced condo percentage gains, signaling renewed buyer interest in this traditional Manhattan property type.

Manhattan Co-op Market Metrics:

-

Median co-op price: $870,000, up 3.6% year-over-year

-

Average co-op price: $1,456,738, up 8.3%

-

Average price per square foot: $1,170, down 1.1%

-

Days on market: 79 days, down 4.8% annually

-

Co-op inventory: 3,669 units, up 5.7%

-

Co-op maintenance fees: $3,054 average monthly, up 8.1% ($2.45/sq ft/month)

These housing costs, including maintenance fees and property taxes, directly impact buyers' purchasing power and overall affordability, especially as rate-driven affordability constraints persist.

More than 60% of Manhattan co-op sales were all-cash purchases, with the cash share rising even higher for premium properties.

Manhattan Co-op Prices by Bedroom Count

Bedroom TypeMedian Sale Price Q3 2025Studio Co-ops$465,0001-Bedroom Co-ops$700,0002-Bedroom Co-ops$1,285,0003-Bedroom Co-ops$2,171,2504+ Bedroom Co-ops$3,875,000Manhattan Luxury Real Estate Market Q3 2025

Luxury Manhattan Condo and Co-op Sales

The Manhattan luxury real estate market (top 10% of sales) showed exceptional strength despite elevated mortgage rates, with 318 luxury sales representing a 13.6% year-over-year increase. Perhaps most notably, luxury inventory declined dramatically while sales grew, a powerful indicator of sustained high-end demand.

Manhattan Luxury Market Metrics:

-

Luxury threshold: $4,000,000 (entry point for top 10%)

-

Median luxury sale price: $5,922,500, up 2.8% year-over-year

-

Average luxury price: $7,891,731

-

Average luxury price per square foot: $2,535

-

Luxury sales: 318 closings, up 13.6% annually

-

Luxury inventory: 1,317 units, down 16.1% year-over-year

-

Luxury months of supply: 12.4 months, down from 16.8 months (26.2% improvement)

The combination of declining luxury inventory and robust sales has resulted in a seller's market for luxury properties.

The luxury segment split:

-

Luxury co-ops: 55.3% of luxury sales, median $4,200,000

-

Luxury condos: 44.7% of luxury sales, median $10,182,995

Manhattan Luxury Real Estate Trends

"In stark contrast to the overall market's 7% inventory growth, the luxury market experienced a 16.1% decline in listing inventory," creating significant upward pricing pressure at the high end. 90% of Manhattan sales above $3 million were cash transactions, demonstrating the financial strength of luxury buyers.

Manhattan New Development Market Q3 2025

New Development Condo Sales Surge

Manhattan new development sales posted exceptional growth in Q3 2025, with 578 closings representing a 71% year-over-year increase, the highest market share for new developments in more than six years.

Manhattan New Development Metrics:

-

New development sales: 578 closings, up 71.0% annually

-

Market share: 18.3% of all Manhattan sales

-

Median new development price: $1,750,000

-

Average price per square foot: $2,206

-

Months of supply: 6.1 months (fastest pace in 3+ years)

-

Inventory: 1,174 units

The surge in new development activity was driven by completions across multiple price points:

-

Sales under $1M: +112.3% year-over-year

-

Sales $1M-$3M: +72.3% year-over-year

-

Sales over $3M: +43.9% year-over-year

New development represented 31.8% of all luxury sales, with a median price of $6,250,000 for luxury new development units.

Limited new development and supply constraints are expected to persist over the next few years, maintaining a tight market outlook.

Manhattan Real Estate Market Trends and Conditions

Sales Activity and Market Velocity

Manhattan real estate sales velocity increased significantly in Q3 2025, with the market posting its third consecutive quarter of year-over-year sales growth. The 3,158 closings came in 4.3% higher than the 10-year Q3 average of 3,029 sales, demonstrating that current activity exceeds historical norms.

Notably, Manhattan has now experienced six consecutive quarters of positive contract activity or sales growth, underscoring the market's durable performance.

Market velocity indicators:

-

Days on market: 77 days (from last list date), down 3.8% annually

-

Months of supply: 7.3 months, down 6.4% year-over-year

-

Listing discount: 6.2% (consistent with 10-year average of 5.9%)

-

Bidding wars: 4.7% of sales (down from 9.7% last year)

“It’s not blazing, but the market is slowly getting faster,” according to report author Jonathan Miller.

Manhattan Real Estate Inventory Levels

Total Manhattan housing inventory reached 7,733 listings at quarter-end, up 7.0% year-over-year. However, because sales grew faster than inventory (+13.4% vs. +7.0%), the market continued to tighten throughout the quarter.

This marked the third consecutive quarter where sales outpaced inventory growth, creating sustained upward pressure on Manhattan real estate prices across all property types.

Inventory breakdown:

-

Resale inventory: 6,559 units (+9.1% YoY)

-

Co-op inventory: 3,669 units (+5.7% YoY)

-

Condo inventory: 4,064 units (+8.3% YoY)

-

New development inventory: 1,174 units (-3.1% YoY)

-

Luxury inventory: 1,317 units (-16.1% YoY)

Note: The inventory figures above are for reference only and may be subject to change as new data becomes available.

Cash Buyers Dominate Manhattan Real Estate Market

Record Cash Transaction Levels

Cash purchases continued to dominate the Manhattan real estate market in Q3 2025, representing 65.3% of all transactions, well above the 10-year average of 52.2%. This cash dominance reflects buyers with substantial resources navigating elevated mortgage rates.

Cash vs. financed buyer trends:

-

Cash buyers increased 31% year-over-year

-

Financed buyers decreased 9.2% annually

-

90% of sales above $3 million were cash transactions

-

Cash share of luxury sales remained elevated throughout the quarter

The shift toward cash buyers accelerated following the rise in mortgage rates of more than 50 basis points since early August 2025. Well-capitalized purchasers, including trade-up buyers with substantial home equity, continued to drive market activity.

Manhattan Condo and Co-op Price Trends

Overall Manhattan Real Estate Pricing

For the third consecutive quarter, both median and average Manhattan real estate prices rose together, a pattern not consistently seen since 2022. This dual appreciation across price metrics indicates broad-based market strength.

Manhattan price metrics Q3 2025:

-

Overall median price: $1,180,000, up 5.8% year-over-year

-

Overall average price: $1,989,107, up 0.8% annually

-

Average price per square foot: $1,552

-

Resale median price: $1,026,500, up 2.7% annually

Price Appreciation Drivers

Several factors contributed to Manhattan real estate price appreciation in Q3:

-

Sales mix shift: Properties over $2 million rose at triple the rate of sub-$2M sales

-

Luxury strength: High-end sales pushed overall median prices higher

-

Inventory constraints: Supply growing slower than demand in key segments

-

Cash buyer dominance: Well-capitalized buyers less sensitive to pricing

Manhattan Real Estate Market Forecast Q4 2025 and Beyond

Near-Term Manhattan Market Outlook

The Manhattan real estate market enters Q4 2025 from a position of considerable strength, though several factors will influence near-term performance:

Positive indicators:

-

Year-to-date sales up 18.7% through Q3

-

Sales running 4.3% above 10-year averages

-

Luxury inventory constraints supporting high-end pricing

-

Sustained cash buyer presence providing market stability

-

Months of supply faster than decade norms

Considerations:

-

Mortgage rates rose 50+ basis points since early August

-

Impact of rate increases not yet fully reflected in demand

-

Mayoral election creating some uncertainty (though limited impact on market fundamentals, as housing policy falls under state authority)

2026 Manhattan Real Estate Projections

"If mortgage rates stabilize or decrease by year's end, a rise in sales next quarter seems likely," according to the Douglas Elliman report. The fundamentals driving Manhattan's market, employment strength, limited new supply, and its position as a global financial center, remain intact.

Key factors supporting 2026 outlook:

-

Supply constraints: New development inventory at lowest levels in years

-

Luxury momentum: Severe inventory shortage in high-end segment

-

Cash cushion: Two-thirds of buyers paying cash reduces rate sensitivity

-

Historical resilience: Manhattan has consistently outperformed national trends

-

Pent-up demand: Financed buyers waiting for improved rate environment

Manhattan Neighborhoods and Submarkets

While this Q3 2025 report focuses on Manhattan-wide trends, significant variation exists across neighborhoods. Premium areas including the Upper East Side, Upper West Side, Tribeca, SoHo, and the West Village continue to show particularly strong luxury condo and co-op performance.

Buyers and sellers seeking detailed neighborhood-specific Manhattan real estate analysis should consult with experienced local brokers who can provide granular market insights for specific buildings and streets.

Manhattan Real Estate Market: Key Takeaways

The Manhattan condo and co-op market delivered exceptional Q3 2025 performance:

-

Sales Surge: 3,158 closings (+13.4% YoY) reached highest level in 2+ years

-

Broad-Based Growth: Both condos (+16.6%) and co-ops (+11.0%) posted double-digit gains

-

Price Appreciation: Third consecutive quarter of median and average price increases

-

Luxury Strength: High-end sales up 13.6% while inventory down 16.1%

-

Cash Dominance: 65.3% of all sales and 90% of sales over $3M were cash

-

New Development Boom: 71% sales increase, highest market share in 6+ years

-

Market Velocity: Days on market down, months of supply improving

-

Above-Average Performance: Sales running 4.3% above 10-year norms

About This Manhattan Real Estate Market Report

This comprehensive Manhattan condo and co-op market analysis is based on the Q3 2025 Douglas Elliman Real Estate Market Report, prepared by Miller Samuel Real Estate Appraisers & Consultants. The report analyzes closed sales data for Manhattan condominiums and cooperatives, providing the most accurate picture of current market conditions.

For personalized Manhattan real estate insights, neighborhood-specific analysis, or to discuss buying or selling opportunities in the current market, please contact me directly.

Best Regards,

Anthony

Data Source: Douglas Elliman / Miller Samuel Q3 2025 Manhattan Sales Report

Last Updated: June 8, 2026

Frequently Asked Questions

What is the median price for a Manhattan condo in Q3 2025?

What is the median price for a Manhattan co-op in Q3 2025?

How many Manhattan real estate sales closed in Q3 2025?

What percentage of Manhattan real estate sales are cash?

What is the luxury threshold for Manhattan real estate?

How is the Manhattan new development market performing?

Domestic relocators are reshaping both coasts. See how it's playing out in Miami.

Recent Reports

Manhattan Market Report - Q2 2025 Sales Hit 2-Year High While Buyers Favor Cash Market Conditions The Manhattan real estate market continued its rebound in Q2 2025, with closings reaching…

Sales Hit 2-Year High While Buyers Favor Cash

Market Conditions

The Manhattan real estate market continued its rebound in Q2 2025, with closings reaching their highest level in nearly two years. A total of 3,042 sales closed, marking a 16.6% year-over-year increase and coming in 8.4% above the 10-year quarterly average. This was the third consecutive quarter of annual price growth following last year’s declines. Notably, however, about half of the deals were signed before April, ahead of the rollout of the new U.S. tariff policy, which may have helped boost the quarter’s numbers.

Contracts Signed

Unlike closed sales which for the most part depicts the past, contracts signed is a leading indicator of the real estate market. Shaking off the uncertainty over tariff policy, Contracts Signed in June 2025 saw a strong surge in newly signed contracts across all property types:

- Co-ops: 506 contracts, up 27.5% YoY

- Condos: 354 contracts, up 17.6% YoY

- 1-3 family homes: 31 contracts, up 106.7% YoY

Luxury demand remained the standout. Signed contracts in the $5M-$9.99M and $10M-$19.99M price bands jumped significantly. For example, condo contracts in the $10M-$19.99M range more than doubled year-over-year. According to the Douglas Elliman Market Report, luxury contract volume (the top 10% of the market) has more than doubled in the past two months alone.

Cash Dominates

Cash purchases hit a record-high 69.1% of all sales.

- 78.3% of sales over $3M were cash- 60.4% of sales under $1M were cash (well above the historical average of 43.3%)

- Financed sales rose only 5.7% year-over-year, while cash deals surged 23%, reflecting tighter lending standards and a more competitive all-cash buyer pool.

Inventory & Months of Supply

Listing inventory ticked up 3.1% to 8,296 units, but it was outpaced by rising sales, reducing the months of supply to 8.2, down from 9.2 a year ago and just below the decade average of 8.3 months.

New Development

The strength in new development was driven by end-users rather than investors, with foreign buyers comprising just 6.5% of all sales, well below the decade average of 11.7%.

- Closings: 408, up 19.3% YoY

- Median sale price: $2.31M, up 13.1%

- Average unit size: 1,563 SF, up 13.3%

- Discount: Improved to 3.6% from 6.3%

- Market share: 13.4% of all closings

Luxury Market (Top 10%)

Luxury performance continues to outpace the broader market, supported by cash-heavy buyers and a tightening supply of ultra-high-end listings.

- Entry threshold: $4.5M

- Median price: $6.525M, up 8.8%

- Average price: $8.57M

- Sales: 310, up 18.3% YoY

- Inventory: Down 21.2%

- Months of supply: 12.1, improved from 18.2

- Listing discount: 8.2%

- Days on market: 133 days, up from 94 a year ago

Resale Market

- Closings: 2,634, up 16.2% YoY

- Median resale price: Flat at $1.05M

- Listing discount: 6.0%, cut in half from last year

- Inventory: 7,119 units (+4.7%)

- Months of supply: 8.1, down from 9.0

Manhattan Remains Resilient

Manhattan's real estate market remains resilient, bolstered by strong demand, limited new development, and a high proportion of cash transactions. In times of global market volatility, investors have historically shifted capital from equities to tangible assets like prime real estate, seeking stability and long-term value. While headwinds of tariff uncertainty and high mortgage rates remain, Manhattan is entering this phase from a position of strength.

Key Market Indicators:

- Population Growth: Net population and international migration to New York City have been on the rise.

- Inventory Constraints: The supply of available properties remains insufficient to meet demand.

- Price Appreciation: Property prices continue to climb across all market segments.

- Return to Office: Placer.ai's April 2025 Office Index indicated that New York City office foot traffic was just 5.5% below April 2019 levels, the smallest drop among major U.S. cities.

For personalized insights or to discuss opportunities in the current market (buyers and sellers), please reach out.

Best Regards,

Anthony

May 2025 Manhattan Pre-Tariff Q1 2025 Results & Early Q2 Momentum 🏙️ Manhattan Market Resilience Amid Global Trade Developments The first quarter of…

Manhattan Pre-Tariff Q1 2025 Results & Early Q2 Momentum

🏙️ Manhattan Market Resilience Amid Global Trade Developments

The first quarter of 2025 marked Manhattan’s strongest performance in years, before President Trump’s sweeping tariffs were announced in early April. While market watchers have been waiting to see how the tariffs might impact demand, the data through early May confirms that the market remains steady and active, not speculative or collapsing.

📊 Q1 2025, A Market on the Move

The first quarter of 2025 showcased a robust Manhattan real estate market, characterized by increased sales activity, rising prices, and strong demand across various segments.

Strongest Quarter in Three Years:

Nearly 2,560 closings, up 28.8% year-over-year, with improvements in sales, supply, and days on market. Only the fourth time this has happened in 20 years.

Sales Outpaced Modest Supply Growth:

Listing inventory rose just 7.5%, supporting a faster pace of deals and stronger pricing.

Manhattan Luxury Real Estate Market Performance:

Price trends for the luxury segment were higher than the overall market. Sales of luxury properties (top 10% of the market) jumped 37% year-over-year, with the average luxury home price reaching $10.3 million, the highest on record. The Entry level price for Luxury was $4.4M, up 19.7% from the previous year and the price per square foot was $3,173, up 16%.

Healthy Price Metrics:

A sales mix shift to larger units, a higher share of new development sales (13% vs 9.7%; which, generally are more expensive than resales), and more higher end sales pushed price trends higher.

- Average Sales Price: $2.2 million, up 21%

- Median Sales Price: $1.17 million, up 11%

- Condo Average Sales Price: $3.1 million, up 17%

- Condo Average Price PSF: $2,130, up 10%

- New Development Average Sales Price: $3.95M, up 21.4%

- New Development Average Price PSF: $2,563, up 9%

Financing Remains Conservative

- 58% of all sales were cash deals, rising to 90% for homes priced over $3 million.

- High lending standards and low default rates continue to characterize the market.

Supply Constraints Persist

- Very low new development pipeline in Manhattan since Covid due to high materials and financing costs and regulatory hurdles.

- Government incentives like the new 485x tax abatement remains underutilized because stringent requirements and high associated costs have led to limited adoption by developers.

- Homeowners are discouraged from moving because they are locked into low mortgage rates. This reduces housing supply for sale and, ultimately, sales activity. Currently, 73.3% of US mortgage borrowers have rates below 5.0%, significantly lower than current market rates, which average around 6.76% for a 30-year fixed mortgage.

📈 April 2025, Manhattan Market Held Strong Even After Tariff Announcement

April 2025 Signed Contracts were 1,150, up across the board compared to April 2024.

- All transactions: +11%

- Condos: +8%

- Co-ops: +13%

Mid Market Led Growth Compared to April 2024

- Contracts between $2M - $3M rose 24%

- Greater than $5M rose 3%

Inventory Gains Enabled Sales Activity

- Active listings rose 16% compared to March but were down 1% compared to April 2024.

🔍Early May 2025. Manhattan Market Activity Has Been Stable

Despite the uncertainty surrounding tariffs, the first week of May recorded approximately 250 signed contracts, signaling that:

- Buyer engagement remains steady

- The market has not stalled or collapsed.

🏙️ Why Manhattan Real Estate Is Playing Catch-Up

While much of the country experienced double-digit price increases during the pandemic housing boom of 2020-2022, Manhattan was an outlier. As city life paused, offices emptied, and urban migration slowed, prices in Manhattan remained relatively flat or even declined in certain segments while other U.S. markets surged. For many of those markets that shot up, we are seeing some of them deflate now, but not NYC.

What we’re seeing now in Manhattan is a rather healthy recovery as buyers have returned to the city, inventory remains tight, and prices catch up to years of suppressed growth.

🏗️ Tariff Impact on Construction Costs & Prices

With tariffs significantly driving up construction costs, the next wave of Manhattan developments is poised to debut at much higher prices. If building costs go up 25%, a developer is not going to eat this cost, nor is China, Canada or Europe. Realistically, if they can't pass these costs on to buyers, they just won't build.

At a 25% increase in costs, all things being equal, the New Development Average Price PSF of $2,563 PSF (see above) would shoot up to $3,204 PSF for the next wave of new development. For a 2,000 sq. ft. 3-bedroom apartment, that would add $1.2 million to the price for the same exact apartment! Even if the costs went up by half of that in my example (12.5%), that would add $600K to the price.

Mortgage rates fluctuate, but offer refinancing opportunities during the life of ownership. Lower rates, however, are never going to make up the difference in price because of 10-25% tariffs. Therefore, for serious buyers, we suggest securing one of today's new developments at a much lower purchase price than what the next wave might bring. You can always refinance later...

🏡 Conclusion: The Safe Harbor of Manhattan Real Estate

Manhattan's real estate market continues to demonstrate resilience, driven by robust demand, constrained new development supply, and a significant share of cash transactions. Historically, during periods of global market volatility, investors have redirected capital toward tangible assets like prime real estate, seeking stability and long-term value. Despite current uncertainties, Manhattan enters this phase from a position of strength, underscoring its enduring appeal to investors.

- Net Population and International Migration to NYC Has Been Rising

- Inventory Remains Inadequate for Demand

- Prices Continue to Climb Across All Segments

- Hamptons and the Northeast $1M+ Markets Showing Similar Strength

Historical Reports

Five years of Manhattan real estate market commentary, preserved for historical reference. Click any date to expand the full report.

January 2023 Downward Shift in the Manhattan Real Estate Market in Second Half of 2022 The year 2022 was a tale of two markets in Manhattan. Early 2022 continue…

Downward Shift in the Manhattan Real Estate Market in Second Half of 2022

The year 2022 was a tale of two markets in Manhattan.

Early 2022 continued the boom that started at the beginning of 2021, driven by the unleashing of pent up demand and an artificially low rate environment that had been implemented by the Fed at the dawn of Covid.

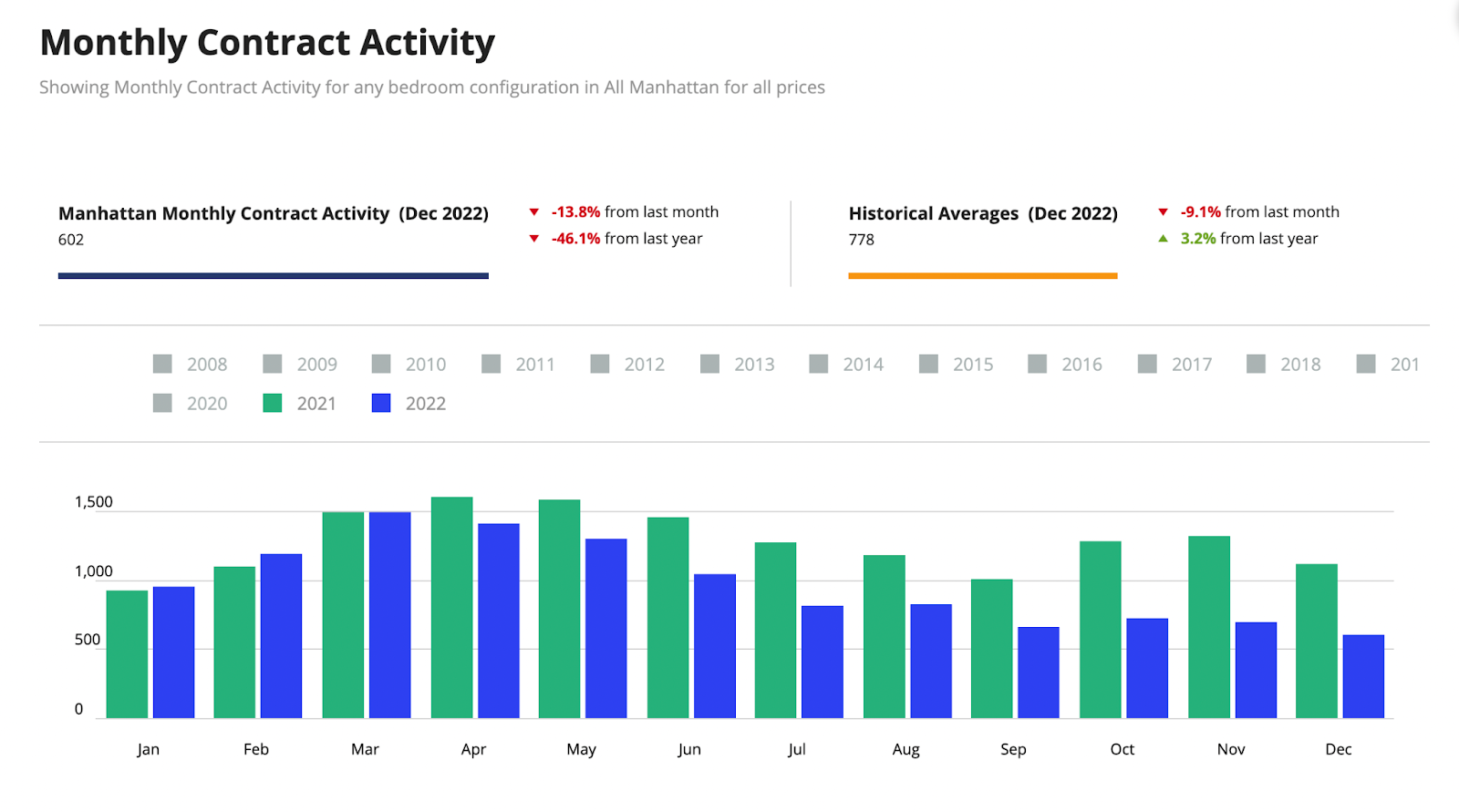

In June 2022, however, after the Fed implemented its first jumbo 75 basis point increase to the benchmark rate, the market quickly softened, leaving most buyers and sellers in a standoff for the remainder of the year as they adjusted to new market realities. This is depicted in the chart below which compares monthly contract activity.

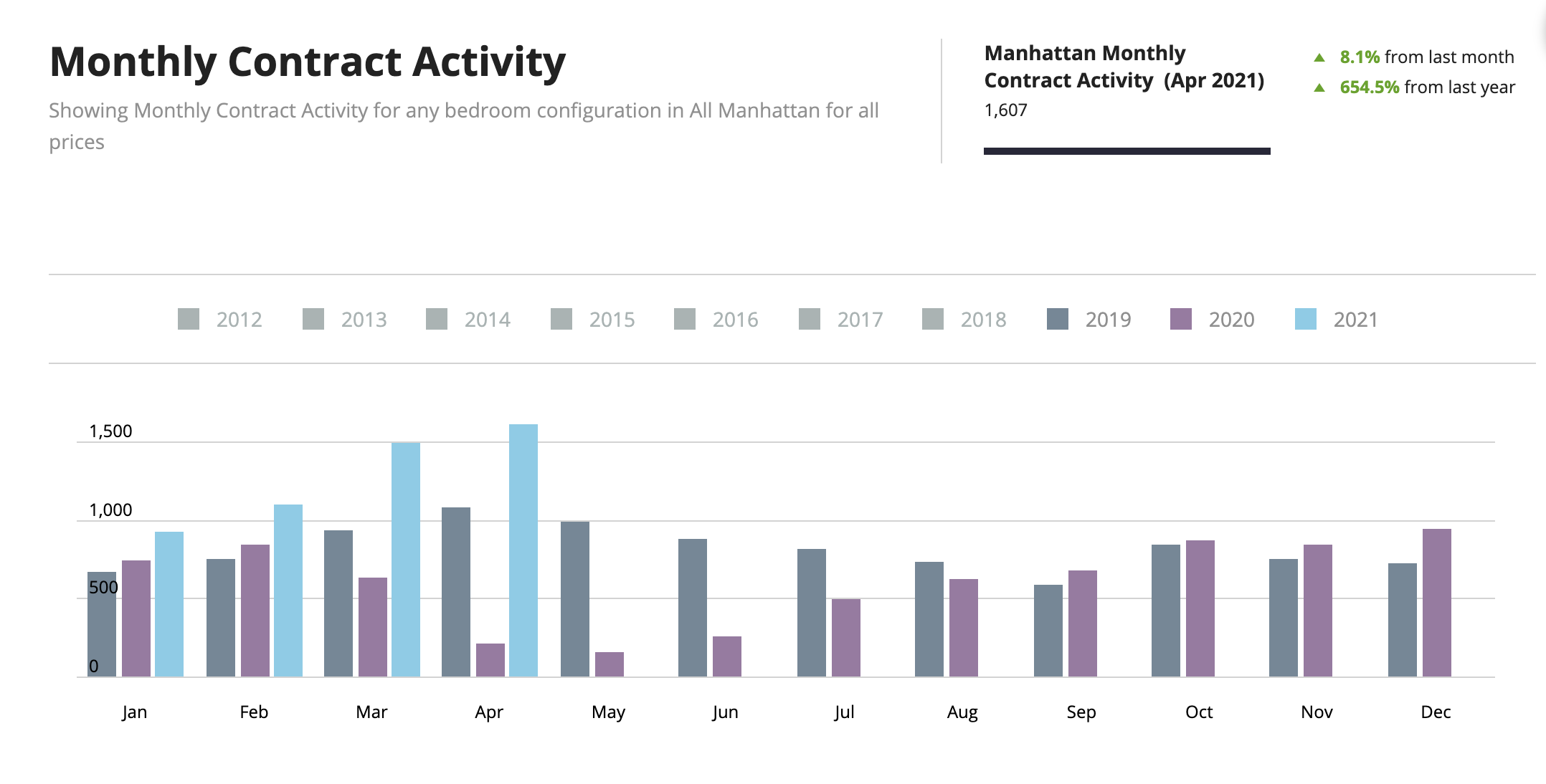

Monthly Contract Activity

With only 602 contracts signed in December 2022, it was one of the worst finishes of the year since 2008. As buyers and sellers come to terms with a new reality, we expect the market to start moving again early in 2023 as there is still demand out there.

Manhattan Property Prices

Condos

- $2.75M average sales price

- $2,074 average price per square foot

- While this was an increase over the same quarter last year, the increase was mainly due to closings happening in a handful of ultra luxury towers, like Central Park Tower and 220 Central Park South, which skewed the results higher.

- Essentially, the price per square foot was flat year to year at just under $2K per square foot.

Coops

- $1.27M average sales price

- $1,225 average price per square foot

New Development

- $3.19M average sales price

- $2,415 average price per square foot

Luxury Segment (top 10% of sales)

- $8.06M average sales price

- $2,909 average price per square foot

- $3.95M entry price threshold for luxury

Fed Rate Hikes in 2022

In the period of only 10 months in 2022, the Fed raised the Feds fund benchmark rate by 4.0%, as shown in the chart below. This unprecedented action was taken to attempt to control inflation, a global phenomenon in 2022.

While the rates are higher than they have been since 2008, they have been high before and real estate markets worked fine in that type of rate environment. However, the pace of the rate increases this year, compacted into only 10 months, is what is most concerning. This has translated to the 30 Year Fixed Jumbo Mortgage rate increasing from 3.1% on January 1, 2022 to 5.7% on December 31, 2022. Down from 6.35% in October.

Manhattan has lots of cash buyers (approx. 55%) compared to other cities, so interest rates don’t alway play such a big part in activity here. In addition, coops, which make up 70% of the inventory stock and are unique to New York City, have very strict rules about the amount of financing one can obtain. Some allow 70% maximum financing, but many only allow 50%. Some don’t allow any financing. These are mitigating factors for the NYC market, but don't help the first time home buyer who often require mortgages to purchase.

Manhattan Inventory Supply Saves the Day

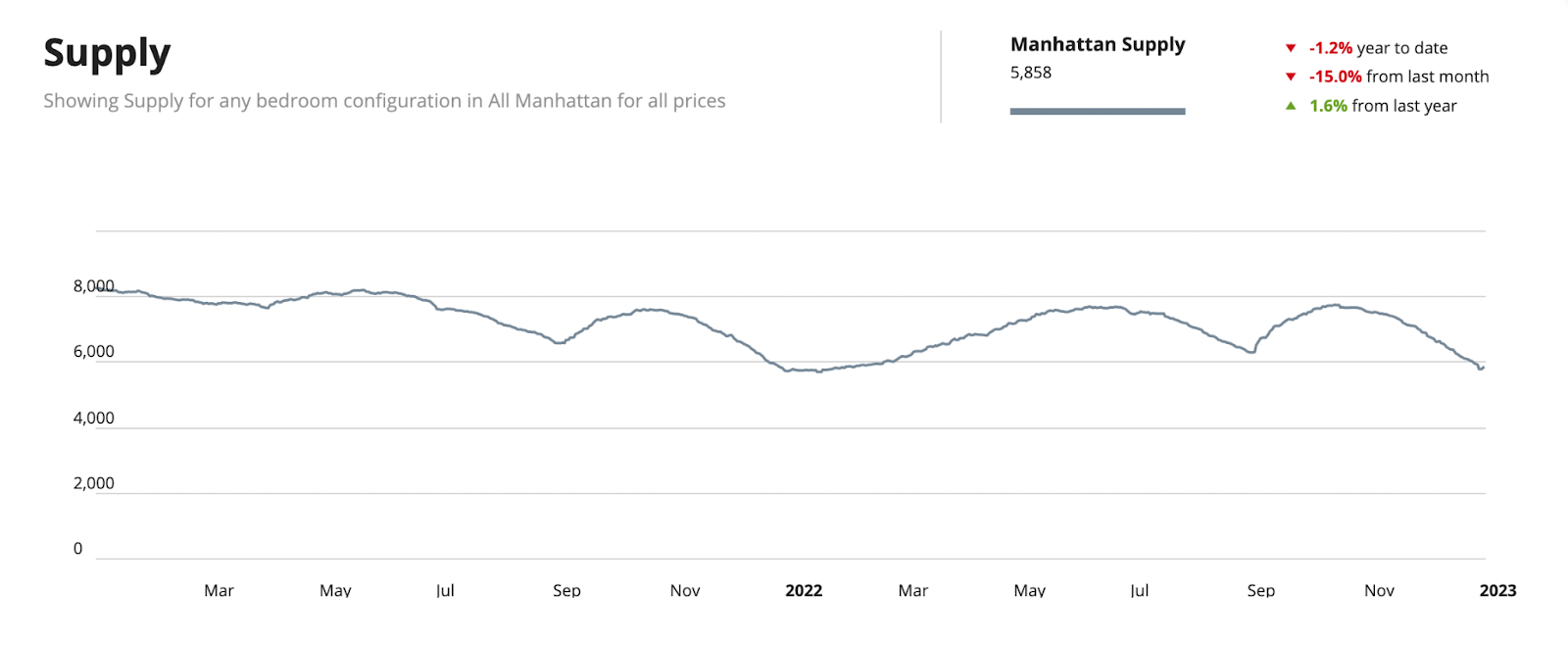

The saving grace in this story is the lack of supply on the market. In comparison to the end of 2020, which had inventory levels over 8,100, today’s supply is at a low of 5,858. There are many reasons for this, as I discussed back in August and summarized below.

The limited amount of supply should put a floor under potential price declines as we go into 2023. And, we don’t see any inventory coming on the market any time soon either because of the following reasons:

- Golden handcuff mortgages

- 80% of New Yorkers with mortgages have rates less than 5%.

- This will result in owners staying in their current homes indefinitely.

- No one is going to trade their 3% mortgage for a 6% mortgage any time soon.

- Frozen rental-to-condo conversion market due to 2019 NY State law

- The law penalizes building owners that have rent stabilized tenants making it impossible to ever create market rate apartments out of rent stabilized units. Unless a change is made to this law, there will be zero conversions as they don’t make any financial sense for a developer.

- Expiration of tax abatement programs make it more expensive for developers to build

- The 421a, 421g, J-51 abatements all expired.

- These were once great tools that the government used to get developers to build but no longer exist.

- Leftist NYC politicians have been vetoing projects with generous 30% and 50% affordable housing components

- Few Manhattan land sales in the last two years, so not very many developers are planning to build in the city.

- Inflation put the brakes on many developments, as costs are not known, like in normal times.

Manhattan Real Estate Outlook 2023

Many forecasters have predicted home prices falling across the world over the next year. This will likely happen, however, mainly in those places that had the highest drive up in prices during Covid. In the US, many smaller cities are at the highest risk as those are where prices rose the most. Places like Boise, ID, Salt Lake City, UT, Phoenix, AZ and all of Connecticut it seems.

New York City, however, was not one of these places. In fact, New York City prices declined during Covid as there was a mass exodus of the city at the beginning of Covid. Prices only recovered those losses in 2021 and posted modest increases in comparison to most other cities.

Knight Frank’s Prime Residential Forecast expects Manhattan prices to rise at least 2% in 2023 behind Miami (5% increase) and Los Angeles (4% increase) in the US. That level of increase places Manhattan in 13th place in their forecast of the top 25 global cities, demonstrating resilience and confidence in the city (and the US in general).

Knight Frank cites “safe haven capital flight” and “overseas buyers…seeking more, rather than less, exposure to the US Dollar.” No doubt, the factors I note about low supply will help offset downward price pressure from Fed actions in 2023.

July 2022 Manhattan Property Market Will See Continued Strength A lot of people have been asking us about what we think is going to happen in the NYC market now that the Fed has raised rates. While activity has slowed do…

Manhattan Property Market Will See Continued Strength

A lot of people have been asking us about what we think is going to happen in the NYC market now that the Fed has raised rates. While activity has slowed down, the Manhattan market remains active based on historical measures.

Many people have been asking whether the slow down will bring price declines. While some experts are saying this will definitely happen in some regions of the country, given how fast prices went up in those regions, they are expecting the odds of price declines in Manhattan to be Low risk.

CoreLogic Analysis. June 2022: Probability Prices will Decline

According to CoreLogic, metro NYC has a Low probability of seeing price drops over the next 12 months.

Manhattan

Prices

Prices didn’t rise at the same rate as other locations across the country. The property market crashed in 2020 (with prices declining, on average 7%) and only started rebounding in Q1 2021, once vaccines were out (with prices rising on average 16%).

- Considering prices in Manhattan rose 4.5% per year over the last 10 years, a net increase of 9% (16% less 7%) is about the equivalent of 2 years of normal price growth.

- Rental rates are up 20% year-over-year causing yields to spike, making it a great time for investors to buy Manhattan property (especially since prices didn’t spike).

- We expect Manhattan rental rate hikes to continue, as mortgage rates cause less first time homebuyers to buy in the coming 12 months and forcing more people into the rental market.

- Manhattan’s high property prices continue to be supported by high local incomes, as the UBS Global Bubble report has consistently reported.

- Manhattan is a long term play. Investors buy Manhattan property for safety. Given the costs involved, it is not a place for naked speculation or flipping.

- 50% of Manhattan buyers pay cash for their property purchases, especially in the luxury segment, so they are not as affected by shifting interest rates.

- Coops make up 75% of housing stock. Many Coops don’t allow financing or limit it to 50%. This fact buoyed Manhattan real estate during the Lehman crisis.

- However, underwriting is very strict so this is not a 2008 scenario.

Supply

- Supply is relatively low for the best NYC condo projects in prime areas.

- Supply is down 10% over the same month last year.

- Looking at Luxury Condos, there are very few of them in the Pipeline.

- Every now and then we get requests from investors looking for bulk condo deals in Manhattan. In 2018, there were quite a few and lots of buildings with at least 50 units to sell.

- In preparing a recent analysis for two separate investors (one doing a very large 1031 transaction), however, I noted that there are very few stellar buildings coming on the market in the next 3-5 years below 96th St. And, the number of buildings with more than 50 units to sell dropped significantly compared to four years ago.

- Some buildings that were sitting in the pipeline that we were anxiously awaiting, like The Cortland, One High Line and One Wall Street have commenced sales. These are all very high-end projects. Beyond these, there are few top condos coming in prime areas.

- The lack of supply of quality product will likely push up prices further, until there is a demand and supply equilibrium. This will likely take years.

- The expiration of the 421a tax abatement, which, in the past had incentivized developers to build condos and rental buildings, has led to fewer new developments in the pipeline.

- New York’s liberal politicians don’t have the appetite to incentivize developers to build, so we don’t see this incentive coming back.

- Of course, these politicians are short sighted. The lack of incentives to developers will only a) reduce the amount of affordable housing being built (a requirement for new construction projects in Manhattan), b) reduce revenues for the city and state, and c) further increase rental rates for tenants.

Headlines and Averages

I always enjoy listening to Leonard Steinberg of Compass. In a recent post, he warned buyers and sellers not to believe the headlines and not to look too much at the averages. And he is definitely right.

- Real estate is hyper-localized.

- Don’t confuse headlines in one market (or across the country) with another market.

- Manhattan is a truly unique market (for many reasons) and national trends don’t apply, as history has shown us.

- In Manhattan, we see how hyper local the market can be. Here we assess buildings individually, as often neighboring buildings can have totally different pricing, totally different demand, totally different trajectory, etc.

Therefore, don’t get caught up in the averages, as the averages only tell us about what happened in the market as a whole and essentially nothing about what happened in a particular building (or line of a building, for that matter).

We are here to help you navigate through the Manhattan market. Schedule a quick call with me if I can shed light on anything else you are contemplating. I would be happy to discuss the market in further detail, provide a valuation for your home if you are thinking about selling, or send you a search of properties.

Happy Summer!

Anthony Guerriero

October 2021 Blockbuster Manhattan Real Estate Market Continues into Q3 2021 The year 2021 will undoubtedly be one of the best years in residential real estate in Manhattan’…

Blockbuster Manhattan Real Estate Market Continues into Q3 2021

The year 2021 will undoubtedly be one of the best years in residential real estate in Manhattan’s history, topping $9.5B in closed sales in the third quarter alone, the most closed sales in one quarter in 32 years.

Sales activity was spurred by unleashed pent-up demand, rising vaccine adoption, reasonable pricing, record low-interest rates, a shift to larger spaces (or those with outdoor space), and increased personal wealth.

This $9.5 billion refers to deals that closed in 2021, not necessarily signed in the quarter, which is a more current barometer of the market.

Contracts Signed Down for Summer Season, but Still at Record For the Quarter

As you can see by the chart below, contracts signed activity has been at elevated levels since the beginning of the year, although it has been tapering off. Such tapering could be a result of seasonality, as summer months are usually slower than the rest of the year. That being said, sales for the quarter were record breaking.

While 29% lower than the previous quarter, 3,500 deals were signed in the quarter. At 270 deals per week in the quarter, that is a record breaking number. October continues the trend, clocking in approx. 305 deals a week.

Sellers are Happy, but Not Too Happy

Sellers in 2021 have been very happy, especially after a dearth of sales in 2020. Buyers are out there, so demand is very strong, especially in the luxury segment where you will find the larger apartments.