In Short

NYC's 421-a tax abatement reduces real-estate taxes 25-100% for new residential construction across 10/15/20/25-year tiers. While the original 421-a expired in 2022, replacement program 485-x took effect in 2024. Existing 421-a abatements continue through their original terms — many active until 2042-2045. Notable buildings include 35 Hudson Yards, One High Line, 111 West 57th, and Central Park Tower. Buyers should always verify the remaining term on every condo resale.

Executive Summary

- 421-a is the dominant NYC condo tax abatement — 25-100% real-estate tax reduction across 10, 15, 20, and 25-year terms. Original program expired June 2022; existing abatements survive through their full terms.

- Replacement program 485-x took effect 2024 — designed for affordable-housing partnerships. Most ultra-luxury condo deliveries since mid-2022 do not carry tax abatements.

- Active 421-a buildings include 35 Hudson Yards, One High Line, 111 West 57th, Central Park Tower — abatements running through 2042-2045. On a $5M condo, tax savings can exceed $400,000 over the abatement period.

- Co-op buildings rarely benefit from 421-a since they're seldom new construction. Co-ops receive separate condominium / cooperative tax abatement and STAR credit benefits.

- Always verify remaining abatement term at resale — abatements transfer with the unit but the term continues from the original delivery date, not the resale date.

NYC tax abatement programs are being phased out. The 421-a program expired in June 2022 and its replacement (485-x) effectively excludes Manhattan condominiums. For the full 2026 NYC tax stack — mansion tax, transfer taxes, mortgage recording tax, FIRPTA, capital gains, 1031 exchange, and the current state of abatements — see NYC Real Estate Taxes & Abatements.

Updated December 2025

Key Takeaway: The 421-a tax abatement program expired in June 2022, meaning no new Manhattan condos can receive these benefits. However, buildings that secured exemptions before the deadline—including One Manhattan Square, Waterline Square, Hudson Yards, One West End Avenue, One Riverside Park, 242 Broome, The Kent, and Brooklyn Point—continue to offer buyers significant tax savings through the 2030s and beyond.

What Is a Tax Abatement in NYC Real Estate?

A tax abatement is a property tax exemption or reduction that lowers your annual carrying costs for a set period, typically 10 to 35 years. In New York City, the 421-a program offered developers tax breaks in exchange for building affordable housing—and those savings were passed along to condo buyers.

Example: A $2.7 million two-bedroom at The Kent on the Upper East Side could generate approximately $300,000 in tax savings over 12 years during the full exemption period—not including additional savings during the 8-year phase-out.

For investors focused on maximizing yield, these reduced carrying costs directly improve net operating income and overall profitability.

How Does the 421-a Tax Abatement Work?

The 421-a tax abatement reduces property taxes on qualifying new construction in New York City. Here's how the most common structures work:

| Abatement Type | Full Exemption Period | Phase-Out Period | Total Duration |

|---|---|---|---|

| 20-Year 421-a | 12 years at 100% | 8 years (taxes increase 20% every 2 years) | 20 years |

| 25-Year 421-a | 21 years at 100% | 4 years phase-out | 25 years |

| 35-Year 421-a (Rental) | 25 years at 100% | 10 years partial | 35 years |

Important: When you purchase a resale unit in a 421-a building, you inherit the remaining abatement period tied to the building's certificate of occupancy—not a fresh 20 or 25 years.

Why Did the 421-a Program End?

The 421-a tax abatement program expired on June 15, 2022. New York State legislators allowed it to lapse due to:

- Political pressure from housing advocates who viewed it as a subsidy for luxury developers

- Affordability concerns that the program wasn't creating enough low-income housing

- Wage disputes between developers and construction unions over minimum pay requirements

The program was replaced by 485-x (Affordable Neighborhoods for New Yorkers) in April 2024, which focuses primarily on rental housing and largely excludes Manhattan condominiums.

What Is the 485-x Tax Abatement Program?

The 485-x program, enacted in April 2024, is New York's replacement for 421-a. Key differences include:

- Rental focus: Primarily benefits rental developments, not condos

- Permanent affordability: Affordable units must remain affordable forever (unlike 421-a)

- Higher wage requirements: Projects with 100+ units must pay construction workers $40+/hour

- Extended exemptions: Up to 40 years for qualifying rental projects

- Condo exclusion: Homeownership projects only qualify outside Manhattan with assessed values under $89/sq ft

Bottom line: Manhattan condo buyers cannot benefit from 485-x. The pipeline of new condos with significant tax abatements has effectively ended.

Which Buildings Still Have 421-a Tax Abatements?

Several luxury developments in Manhattan and Brooklyn secured 421-a exemptions before the program expired. These buildings continue to offer substantial tax savings for resale buyers:

One Manhattan Square

| Detail | Information |

|---|---|

| Address | 252 South Street, Lower East Side |

| Developer | Extell Development |

| Completed | 2019 |

| Tax Abatement | 20-year 421-a |

| Remaining Benefits | ~14 years (as of 2025) |

This 80-story glass tower on the Lower East Side waterfront features over 100,000 square feet of amenities including a 75-foot swimming pool, basketball court, bowling alley, Turkish baths, golf simulator, and private theater. Meyer Davis designed interiors with floor-to-ceiling windows and panoramic East River views.

Waterline Square (Upper West Side)

| Detail | Information |

|---|---|

| Address | Riverside Boulevard, W. 59th–63rd Streets |

| Developer | GID Development Group |

| Completed | 2019 |

| Tax Abatement | 20-year 421-a |

| Architects | Richard Meier, Kohn Pedersen Fox, Rafael Viñoly |

Three starchitect-designed towers with 263 condo units sharing 90,000+ square feet of amenities and a 3-acre private park.

15 Hudson Yards

| Detail | Information |

|---|---|

| Address | 15 Hudson Yards, West 30th Street |

| Developer | Related Companies / Oxford Properties |

| Completed | 2019 |

| Tax Abatement | 20-year 421-a |

| Architect | Diller Scofidio + Renfro with Rockwell Group |

The first residential building at Hudson Yards, this 70-story tower connects directly to the retail complex anchored by Neiman Marcus.

35 Hudson Yards

| Detail | Information |

|---|---|

| Address | 35 Hudson Yards, West 33rd Street |

| Developer | Related Companies / Oxford Properties |

| Completed | 2019 |

| Height | 1,009 feet (tallest at Hudson Yards) |

| Tax Abatement | 20-year 421-a |

Includes the Equinox Hotel, 60,000-square-foot fitness facility, and 137 private residences with interiors by Yabu Pushelberg.

The Kent (Upper East Side)

| Detail | Information |

|---|---|

| Address | 200 East 95th Street, Carnegie Hill |

| Developer | Extell Development |

| Completed | 2018 |

| Tax Abatement | 20-year 421-a |

| Remaining Benefits | ~13 years (as of 2025) |

Art Deco-inspired 30-story building with 83 residences, one avenue from the 96th Street Second Avenue subway. Designed by Beyer Blinder Belle with interiors by Champalimaud, the building is located near elite private schools including Dalton, Sacred Heart, and Chapin.

One West End Avenue

| Detail | Information |

|---|---|

| Address | 1 West End Avenue, Upper West Side |

| Developer | Elad Group |

| Completed | 2017 |

| Tax Abatement | 20-year 421-a |

| Remaining Benefits | ~12 years (as of 2025) |

This 42-story luxury tower at the corner of West 59th Street offers panoramic Hudson River views and direct access to Riverside Park South. Designed by Pelli Clarke Pelli Architects with interiors by Jeffrey Beers International, the building features a private motor court, 75-foot indoor swimming pool, and over 20,000 square feet of amenities.

One Riverside Park (50 Riverside Boulevard)

| Detail | Information |

|---|---|

| Address | 50 Riverside Boulevard, Upper West Side |

| Developer | Extell Development |

| Completed | 2015 |

| Tax Abatement | 20-year 421-a |

| Remaining Benefits | Through 2035–2037 |

Another Extell development along Riverside Boulevard, One Riverside Park features 219 residences with interiors by Shamir Shah Design. The building offers over 50,000 square feet of amenities including LA PALESTRA, a 40,000-square-foot athletic club and spa with a 75-foot swimming pool, rock-climbing wall, basketball and squash courts, and golf simulator.

242 Broome (Essex Crossing)

| Detail | Information |

|---|---|

| Address | 242 Broome Street, Lower East Side |

| Developer | Delancey Street Associates |

| Completed | 2018 |

| Tax Abatement | 20-year 421-a |

| Remaining Benefits | ~13 years (as of 2025) |

The first condominium at Essex Crossing, this 14-story building designed by SHoP Architects features 55 residences with interiors by DXA Studio. Kitchens include Calacatta marble countertops, custom walnut cabinetry, and Gaggenau appliances. Residents enjoy direct access to Essex Crossing's 300,000 square feet of retail, the revitalized Essex Street Market, and the Market Line food hall.

Brooklyn Point (Downtown Brooklyn)

| Detail | Information |

|---|---|

| Address | 138 Willoughby Street, Downtown Brooklyn |

| Developer | Extell Development |

| Completed | 2019 |

| Tax Abatement | 25-year 421-a |

| Remaining Benefits | Through 2045 |

Brooklyn's tallest tower at 720 feet, Brooklyn Point offers one of the last 25-year tax abatements available in New York City. Designed by Kohn Pedersen Fox with interiors by Katherine Newman, the 68-story building features 458 residences and over 40,000 square feet of amenities, including the highest residential rooftop infinity pool in the Western Hemisphere. Located atop City Point, residents have direct access to Dekalb Market Hall, Target, and Alamo Drafthouse Cinema. Multiple subway lines (2, 3, B, Q, R, A, C, G) are steps away.

How Much Can You Save with a 421-a Tax Abatement?

Tax abatement savings vary based on property value and building assessment, but the difference is substantial:

| Scenario | Annual Property Tax | 12-Year Savings |

|---|---|---|

| $2.5M condo WITHOUT abatement | $25,000–$40,000 | $0 |

| $2.5M condo WITH 421-a (full exemption) | $2,000–$5,000 | $240,000–$420,000 |

During the phase-out period, taxes increase incrementally:

- Years 13–14: 20% of full taxes

- Years 15–16: 40% of full taxes

- Years 17–18: 60% of full taxes

- Years 19–20: 80% of full taxes

What Should Buyers Know Before Purchasing a 421-a Condo?

1. Calculate Remaining Abatement Years

Abatements are tied to the building's certificate of occupancy date, not your purchase date. A building completed in 2019 has approximately 14 years remaining in 2025—with some of those years in the phase-out period.

2. Plan for the "Tax Cliff"

When the abatement expires, your property taxes will jump to full market rates—potentially increasing $20,000–$50,000+ annually. Smart buyers:

- Factor full taxes into long-term affordability analysis

- Set aside savings during low-tax years

- Consider abatement expiration when planning a future sale

3. Understand the Resale Premium

Studies by the NYC Independent Budget Office found Manhattan condo buyers pay approximately 0.43% of the sales price for each additional year of 421-a benefits remaining. This means:

- Units with more years remaining command higher prices

- The premium diminishes annually as benefits decrease

- Buyers should calculate whether the premium justifies the remaining savings

4. Verify the Building's Specific Terms

Not all 421-a exemptions are identical. Before purchasing, verify:

- Exact expiration date of the building's exemption

- Whether you're in full exemption or phase-out period

- Current year's actual tax bill (offering plans can be misleading)

For the complete 2026 picture across all NYC tax instruments — abatements, transfer taxes, mansion tax tiers, FIRPTA, 1031 — see the master resource: NYC Real Estate Taxes & Abatements.

What Other Tax Abatement Programs Exist for NYC Condo Owners?

Cooperative and Condominium Property Tax Abatement

This annual program provides tax reductions of 17.5% to 28.1% for eligible condo and co-op owners based on assessed value. Requirements include:

- Unit must be your primary residence

- Cannot own more than three units in the same development

- Unit cannot be owned by an LLC or business entity

- Building cannot already receive 421-a, 421-g, or J-51 benefits

- Building must pay prevailing wages to staff

Note: Buildings with 421-a abatements are not eligible. Once 421-a expires, owners may apply for this program.

J-51 Tax Abatement

The J-51 program provides tax benefits for buildings undergoing renovation. Recently revived for buildings with average assessed values at or below $45,000 per unit (approximately $450,000 market value). Primarily used for rental buildings but available to co-ops and condos for capital improvements.

Frequently Asked Questions About NYC Tax Abatements

What is the 421-a tax abatement?

The 421-a tax abatement was a New York City property tax exemption program that reduced taxes on new residential construction for 10 to 35 years. The program expired on June 15, 2022, but buildings that qualified before the deadline continue to receive benefits.

Can I still buy a condo with a 421-a tax abatement in Manhattan?

Yes, but only as a resale purchase in buildings that secured the exemption before June 2022. No new Manhattan condo developments can qualify for 421-a benefits. Buildings like One Manhattan Square, Waterline Square, Hudson Yards, One West End Avenue, One Riverside Park, 242 Broome, The Kent, and Brooklyn Point still offer remaining abatement years to buyers.

How long do 421-a tax abatements last?

Most Manhattan condo 421-a abatements last 20 years: 12 years of full (100%) exemption followed by an 8-year phase-out where taxes increase 20% every two years. Some buildings received 25-year abatements with 21 years at full exemption.

What replaced the 421-a program?

The 485-x program (Affordable Neighborhoods for New Yorkers), enacted in April 2024, replaced 421-a. However, 485-x primarily benefits rental developments and largely excludes Manhattan condominiums.

Do I get a full 20-year abatement when I buy a resale condo?

No. You inherit the remaining years tied to the building's original certificate of occupancy date. If the building's abatement started in 2019 and you purchase in 2025, approximately 14 years of benefits remain.

What happens when the tax abatement expires?

Your property taxes increase to full market rates. For a typical luxury Manhattan condo, this can mean an annual increase of $20,000–$50,000 or more. Plan ahead by factoring full taxes into your long-term budget.

Can I get both a 421-a abatement and the Co-op/Condo Tax Abatement?

No. Buildings receiving 421-a benefits are not eligible for the NYC Cooperative and Condominium Property Tax Abatement. However, once the 421-a expires, owners may apply for the co-op/condo abatement if they meet eligibility requirements.

How do I check if a building has a 421-a tax abatement?

Visit the NYC Department of Finance 421-a Exemption Lookup and search by address or borough-block-lot number. The database shows all properties currently receiving 421-a benefits.

The Future of Tax Abatements in Manhattan Real Estate

The expiration of 421-a represents a fundamental shift in NYC housing policy:

For new development: Without meaningful tax incentives for condo construction, expect fewer new condo buildings in Manhattan. Developers may pivot to rentals (which qualify for 485-x), all-affordable projects, or reduce development activity.

For existing 421-a buildings: These represent a shrinking pool of opportunity. As years pass, remaining benefits decrease, and eventually no Manhattan condos will carry 421-a exemptions.

For buyers: If tax benefits matter to your purchase decision, the window is narrowing. Buildings that secured 421-a before 2022 offer genuine value—but that value diminishes annually.

For the authoritative 2026 NYC tax reference — including the current state of 421-a inventory, mansion tax rates, transfer taxes, and abatement-cliff modelling — refer to NYC Real Estate Taxes & Abatements. This guide is updated quarterly.

Contact a Manhattan Real Estate Expert

Understanding tax abatements is essential for making informed investment decisions in New York City real estate. Whether you're interested in One Manhattan Square, Waterline Square, Hudson Yards, One West End Avenue, One Riverside Park, 242 Broome, The Kent, Brooklyn Point, or other buildings with remaining 421-a benefits, working with an experienced broker can help you calculate the true value of these tax savings.

Manhattan Miami Real Estate

Contact us for personalized guidance on Manhattan condos with tax abatements.

Related Resources

- NYC Department of Finance: 421-a Exemption

- NYC HPD: Tax Incentive Programs

- Cooperative and Condominium Tax Abatement

- Manhattan Condo Market Analysis

- Buying an Apartment in NYC

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Consult with qualified professionals regarding your specific situation. Information current as of December 2025.

Related: NYC Real Estate Tax Topics

The following sections consolidate related Manhattan real-estate-tax topics that previously lived as standalone posts. Content preserved verbatim from the original articles to maintain factual continuity.

Real Estate Taxes vs. Property Taxes — Key Differences

More than likely, you think that real estate tax and property tax are the same things. It's just how most people use the terms interchangeably, which causes some confusion. If you own your own home and a boat, car, or another big-ticket item, you should know the difference. While both types of properties are taxed based on the value of the item, how much you actually pay will depend on whether they're classified as real estate taxes or personal property. If you're still unsure about the differences, that's okay because we'll go into more detail below.

What Are Real Estate Taxes?

When a person owns real estate, they have to pay real estate taxes. To determine how much each homeowner will pay in taxes, you have to multiply a rate that’s been set for the city or municipality by the home’s fair market value. The fair market value of a home can change over time according to the prices that similar homes in the neighborhood have sold for in recent years and any upgrades that have been made to the interior and exterior of the home. If you’ve ever heard of someone not wanting to let an accessor inside of their home because they were afraid that the accessor would value their house higher than what it was currently valued, they’re usually trying to avoid having their real estate taxes go up.

Real estate is defined by the IRS as any kind of land and anything affixed to that land. So if you own hunting grounds or any kind of land, regardless of how you use it and even if there isn't a building on it, that land would be subject to real estate taxes. Additionally, if you own a cabin on that land, it’s subject to real estate taxes and can raise the value of the property as a whole. Additionally, a commercial or industrial building is also subject to real estate taxes. Finally, anything built underneath the property is taxed as real estate. This can include pools, dugout living spaces, fallout bunkers, garages, and almost anything else that you could build underground.

More About How Real Estate Taxes Are Calculated

How a tax rate is determined can depend on where you live. For instance, in New York, the tax rate is determined by taking the rate of at least three different municipalities, counties, towns, or school districts and dividing that by the number of sources that you’re pulling from. This means that the exact tax rate can vary within the same city.

How You Pay for Taxes

When you own a home, you might pay your taxes directly to the IRS, or you might pay your lender, which will pay your tax bill to the IRS on your behalf. If you’ve already fully paid for the home and no longer have a loan, you're more likely to pay your taxes directly to the IRS. Anyone who is in this category of homeowners needs to be especially careful about paying taxes in full and on time to avoid liens on their home and other penalties.

If you have a loan for your home, the taxes are usually tacked onto your monthly loan payment. The lender collects this amount so that they can pay your taxes quarterly to the IRS. If you fail to make the payments to the lender for the real estate taxes, your lender will begin foreclosure proceedings the same way that they would if you were behind on mortgage payments.

What Are Personal Property Taxes?

When you have moveable assets, such as a car, boat, or mobile home, these assets will be subject to property taxes. Like real estate taxes, property taxes are often charged at a particular rate. The total cost of the property taxes that you pay for a moveable asset also depends on the value of the asset in many states. So, for instance, when you have a boat that's valued at $10,000 and a tax rate of 3%, you'll have to pay $300 every year for the personal property taxes on that boat. Having an updated assessment of the value of your personal property can save you money on your taxes because the value of many types of moveable assets tends to go down.

Just like with real estate taxes, if you don’t pay your property taxes in full and on time, you might face fees, liens against the property, and potential seizure of your property.

A Few Exceptions

A general rule of thumb is that if you can move something without it being damaged, it falls into the category of being taxed as property. But if it has to stay in place on land, it’s charged as real estate taxes. A trailer home is classified as personal property if the home is on land that isn't owned by the person who owns the trailer home, such as a trailer home park. In contrast, pre-built homes are considered real property once they're constructed on the property even though they've technically been moved to become part of the property. Most real estate in NYC is unlikely to fall under either of these categories, but there are some neighborhoods where it's possible.

Wrap-Up

Most taxes on a home are taken care of at the sale of the house, but if you’re concerned that you’re not sure of how a particular aspect of the tax system works, you can consult a tax advisor or other professional. It’s also important to remember that falling behind on your real estate taxes isn’t an option, whether you pay your taxes to your lender or pay them yourself at your local tax office. If you end up falling behind, you’ll also subject yourself to the possibility of liens against your real estate and even foreclosure on it.

Capital Gains Tax: Reduction & Deferral on NYC Real Estate

Why give the government more than they are due when you sell your primary home or investment property? There is more than one way to defer, and to reduce, capital gains tax (CGT) when selling property. While it takes planning and following strict government rules, if the circumstances apply, they definitely work.

Our approach combines real estate advisory with a background in accounting, allowing us to evaluate both transaction costs and after-tax outcomes for each client's situation.

When a client sells their property, a primary goal is to maximize the benefits of price appreciation. One of the major costs all property sellers face is the CGT, which is a tax they may owe on appreciation of the property at the time of sale. Astute property owners plan ahead wherever possible to minimize or defer any CGT liability.

Tax liability depends, in many ways, on the seller's specific circumstances. For example, the property may be:

-

A primary residence

-

A secondary or vacation home, or a pied-à-terre

-

An investment property

The property may be owned by:

-

An individual

-

A married couple

-

A corporation or other business entity

Capital Gains Tax liability depends, in many ways, on specifics such as these. The other specific is time. How long someone owns a property also impacts CGT liability. In this article we will discuss specifics and options in general. Everyone who wants specific advice about their own unique circumstances, should consult their US tax accountant. And, if you are a foreigner, then you should consult a tax accountant from your home country who understand implications of tax treaties, if any.

What is Capital Gains Tax?

Capital Gains Tax is a tax levied by the IRS on profits made when, in this context, owned real estate is sold. If the sale results in a loss or a break-even, then no tax is due. However, in most cases there will be capital gains, as property prices tend to rise over time with inflation.

How is "Gain" Calculated and How Can it be Reduced?

The profit, or net capital gain, is calculated by subtracting the property's cost-basis from the net proceeds of the sale. The cost-basis is the cost price paid to buy the property, plus the closing costs incurred to complete the purchase, plus the cost of any permanent capital improvements made to the property during ownership minus depreciation recapture (which we won’t go into here).

Replacing appliances is not a permanent improvement, so cannot be used to increase the cost-basis and reduce the gain. Refitting the kitchen with new cabinets and countertops, however, is considered a permanent improvement and increases the cost-basis of the property (it would offset the capital gain and resulting tax). The cost of repainting the same kitchen is considered maintenance is not capital improvement. Owners should keep all receipts associated with capital improvements to prove their cost-basis should the IRS need confirmation.

The closing costs of selling the property reduces the capital gain. Items such as broker commissions, city transfer taxes, and other direct costs associated with the sale may all be used to reduce the profit figure and so reduce the CGT due.

How Can Time Affect Capital Gains Tax on Real Estate?

Property sold after less than a year result in short term capital gains, which is considered by the IRS to be ordinary income. Often, the tax on the normal income tax on the gain will be much higher than long term capital gains tax rates, depending upon which one of the income tax brackets one would fall in. So, it’s best to own the property for more than one year. If the property is sold for an unexpected and an IRS-approved reason, then the tax liability may be waived or reduced. Reasons include divorce or separation, major illness, losing your job, or suffering a natural disaster, for example.

The Reason for Ownership Affects Capital Gains Tax

A primary residence sold for gain will be subject to limited CGT. A single person may reduce the taxable gain liability by $250,000 before CGT is calculated. A married couple may reduce the taxable gain by $500,000. Capital Gains Tax can, therefore, be reduced by getting married.

If planning to sell your home and it is a second home or vacation home, some forward-planning may pay dividends. The IRS considers a home to be a primary residence if it has been occupied as such for a minimum of two years in the previous five-year period. Establishing a new primary address for mail, voter registration, driver license, etc., two years before selling the property may substantially reduce CGT liability.

Changing every investment property or second home's status to primary residence status before selling will continuously defer up to $500,000 of CGT liability. The IRS does not limit how many times a personal residence may be used to benefit from the tax reduction. This amount of planning may not be possible, so an investor should look at the next route to CGT deferment.

What About Investment Properties?

Selling an investment property for a profit will attract CGT. Fortunately, the government introduced a program so an investor can defer CGT for an unlimited period of time. Specific rules must be followed, but it is another example of how the USA supports property ownership by both domestic and overseas investors.

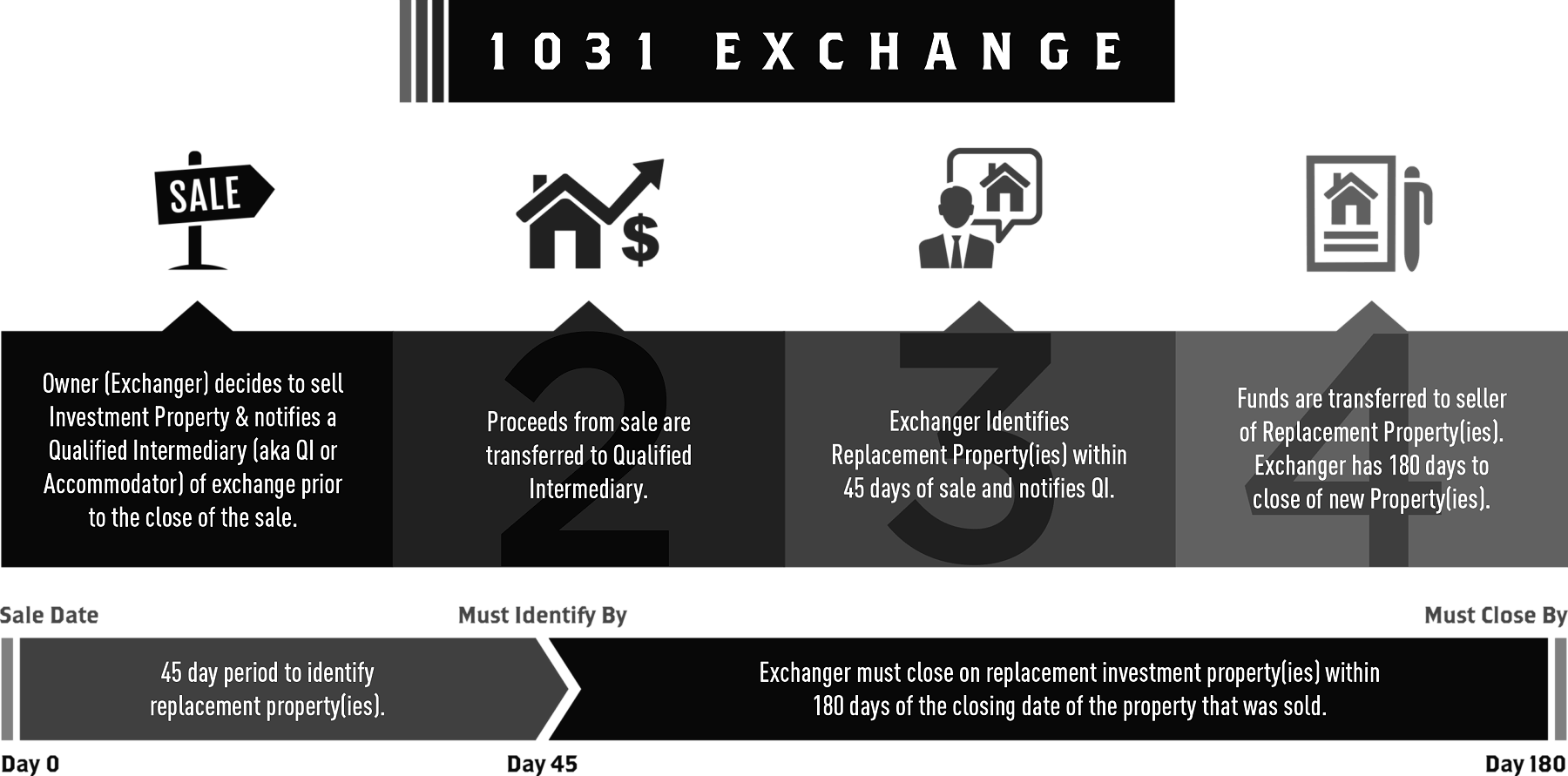

The 1031 Exchange Rules - Tax Deferred Exchange

A 1031 Exchange (also called a Starker Exchange, Like-Kind Exchange, or 1031 Tax Deferred Exchange) enables investors to defer all CGT provided they reinvest the sale proceeds in another approved property. The rules are strict and must be precisely followed, but they also have broad parameters which make deferment easier than it would be. Below are some tips of how to avoid paying taxes when selling a house.

1031 Exchange Process

When an investment property is sold, and all the proceeds are used to purchase another investment property, the CGT liability is rolled over into the next property. When that property is sold, and another purchased, the CGT liability is rolled over again. This can continue forever. At some point, if an investment property is sold, and the profits liquidated, the gain on the sale of that property, alone, will attract CGT which must be paid.

The IRS requires that, for the tax liability deferment to be applied, the next purchase must be "like-kind." This means that if investment real estate is sold, then more investment real estate must be purchased. One Manhattan luxury condo can be sold and more than one lower-cost property in Miami can be purchased.

What matters is that all 1031 Exchange properties are for investment and all the sale proceeds are used to purchase the new "like-kind" property. This means that, for example, a very expensive piece of raw land in Nevada purchased for development but which was never developed could be "exchanged" for a brownstone in Manhattan plus a condo in Miami Beach. One piece of investment real estate property for another piece (or pieces) of investment real estate property or equal or greater value.

Why is it Called an Exchange?

The sale and purchase must be carried out by an approved and qualified intermediary or QI. The QI holds onto the sale proceeds and passes those proceeds to the seller(s) of the replacement property, or properties, without the original seller touching it. So legally, the sale-and-purchase is considered "an exchange." The idea was introduced by Congressman Stalker, and the rules are in Section 1031 of the IRS Code, hence the two names.

What Rules Must a Seller Follow to Defer CGT?

-

All properties must be in the United States.

-

All properties must be "like-kind," so real property cannot be "exchanged" for any stocks and bonds or cash, for example.

-

The purchased (newly acquired) 1031 exchange real estate must be of equal or higher value than the property being sold (relinquished.)

-

The relinquished property must have been used for investment, not any other purpose, and the acquired property must also be intended for investment purposes. (i.e., 1031 exchange nyc residential investment property for 1031 exchange florida commercial property).

-

Time limits, established by the IRS, must be adhered to. The sale and purchase do not have to be simultaneous. This is why a QI manages it all. The QI completes the sale and holds onto all proceeds. The seller then has 45 days to find a replacement property (or properties) and the purchase of the replacements must be completed within 180 days of the earlier sale. The QI will hold the sale proceeds, close on the purchase(s) and transfer the funds without the original property owner having any access to them.

-

The seller may draw up an approved short-list of possible acquisition properties for the QI's records, and then enable their real estate agent to negotiate the purchase so the QI can close the transaction(s).

-

It is acceptable to do a "reverse exchange" which means the investor finds and closes on the acquired property before they close on the relinquished property sale. The QI will explain how that works but what matters is that the investor will still be able to defer CGT when the relinquished property transaction closes.

-

The Exchange Agreement the QI draws up must confirm that all IRS-required steps have been completed correctly and are part of the overall 1031 Tax Deferment plan.

-

If the seller (relinquisher) finances the purchase (acquisition,) the loan must be "appropriate." It must not be large enough to provide a cash surplus to the seller otherwise it negates the exchange, and CGT becomes due.

-

The QI (sometimes called an accommodator) must be in full-time business as an intermediary. The QI must not have any financial relationship with the seller so the QI cannot be the seller's Realtor, CPA, or regular attorney, for example.

That is it. CGT can be minimized and deferred by knowing and following the rules.

A Final Note on "Boot"

1031 Exchanges have their own jargon; relinquish, acquire, intermediary, etc. Another piece of jargon investors hear is the word "boot." This generally refers to any cash received directly from the sale of the property. Meaning cash that did not go thru the QI. As soon as you physically receive cash on the sale that cash is taxable. Therefore, it’s best to surround yourself with advisors, like ourselves, who know all the very strict rules of 1031 exchanges.

Our Approach to Capital Gains Strategy

With a background in accounting, we help clients evaluate the full range of strategies available — from primary residence exclusions to 1031 exchanges to installment sales — and understand how each applies to their specific situation. Every transaction is different, and the right approach depends on property type, ownership structure, and long-term investment goals.

We work closely with each client's tax advisors and legal counsel to ensure alignment across all aspects of the transaction.

Schedule a time to chat with our Managing Broker Anthony Guerriero, MBA, CPA, to discuss your specific situation.

Related Resources

- Net Proceeds Calculator — Estimate What You Keep After Selling

- NYC vs Miami: Comparing Tax and Investment Considerations for International Buyers

Frequently Asked Questions — NYC Real Estate Taxes

Frequently Asked Questions

What is the 421-a tax abatement in NYC and is it still available?

What is the difference between real estate taxes and property taxes?

How can I reduce or defer capital gains tax when selling NYC real estate?

Are NYC condo taxes really frozen for 20 years under 421-a?

Which Manhattan and Brooklyn buildings still offer tax abatements through 2045?

Do co-op owners get the same tax benefits as condo owners?

How does FIRPTA affect foreign sellers of NYC real estate?

What is the NYC mansion tax and when does it apply?

NYC + Miami Real Estate Taxes

Mansion tax, 421-a, FIRPTA, capital gains — both markets.

International BuyersNYC International Buyers Guide

FIRPTA, withholding, ownership structures.

InventoryNYC Co-ops & Condos

Active Manhattan listings with abatement filters.

When you're ready

Begin with a conversation, not a listing.

Manhattan Miami advises buyers and sellers across both markets. We start by understanding your goals — then we curate the right buildings, neighborhoods, and timing.

Start the Conversation421-a Active NYC Condo Buildings Through 2042-2045

Curated by Manhattan Miami · 2026 data

Notable 421-a Buildings Still Under Abatement — Verified at Resale

| Building | Neighborhood | Abatement Tier | Term Remaining | Active Resale Range |

|---|---|---|---|---|

| Central Park Tower | 57th St / Billionaires Row | 20-year | Through ~2045 | $10M-$250M+ |

| 111 West 57th | 57th St / Billionaires Row | 20-year | Through ~2042 | $8M-$70M |

| One High Line | West Chelsea | 20-year | Through ~2043 | $5M-$45M |

| 35 Hudson Yards | Hudson Yards | 20-year | Through ~2042 | $5M-$60M |

| The Cortland | West Chelsea | 20-year | Through ~2044 | $2.75M-$25M |

| 520 Park Avenue | Upper East Side | 20-year | Through ~2040 | $15M-$130M |

| 432 Park Avenue | Midtown / Park Ave | 20-year | Through ~2036 | $7M-$95M |

| One57 | 57th St / Billionaires Row | 10-year+10-year | Through ~2032 | $4M-$100M |

| 15 Hudson Yards | Hudson Yards | 20-year | Through ~2041 | $4M-$30M |

| 56 Leonard Street | Tribeca | 15-year | Through ~2031 | $3M-$50M |

Active inventory: Miami pre-construction, Billionaires' Beach Miami.